Lately we’ve been reporting how little interest there has been in purchasing gold and silver in recent months. This article from John Kim backs this up and expands upon why the demand to buy gold from retail buyers is always so low at times like this.

He also looks at why the Chinese movement to take more control over the setting of prices in the physical gold and silver markets is likely to be a “slow burn” process and will not lead to a massive spike in precious metals prices…

Interest in Gold and Silver is Always Lowest When Opportunity is Best

By JS Kim

Managing Director

Earlier, in February/March of this year, on my SKWealthAcademy SnapChat channel, I warned daily of potential deep pullbacks in the asset prices of gold and silver that then materialized. In mid-March as gold/silver prices recovered, I wrote a blog article, here, titled, “Expect Divergences, Not Convergences, Between US Stock and PM Asset Prices for the Remainder of the Year.” This too has manifested, almost to perfection, thus far. As you can see from the chart below, after I posted that article, gold and silver mining stocks rose and US stocks fell. Then US stocks rose and gold and silver mining stocks fell. Will this relationship remain for the rest of 2017 as I predicted? Maybe not as perfectly as the below chart illustrates, but I still believe that this relationship will hold true in general for the rest of the year.

However, what is much harder to fathom, are the excessive amounts of pessimism that surround gold and silver assets at this current time, when quite a strong buying opportunity exists. Though the enormous volatility of PM mining stocks this year has of course contributed greatly to this pessimism, as people have a strong distaste for uncertainty, if we step back, just for a second, and look at the greater picture, there should not be, in my opinion, this much pessimism surrounding gold and silver at this time, especially when you compare yields of gold versus US stock markets over a longer period of time. Again, from a close-up view, if we look at spot gold prices, it’s been a rollercoaster ride, though volatility in physical gold prices has been fairly muted this year, due to growing premiums of physical prices over paper prices, which illustrates the necessity of holding physical gold and silver over their banker-controlled paper derivatives. Gold dropped sharply in March, then rose sharply for about four weeks, and then dropped sharply again from mid-April onward, falling roughly $80 an ounce over 18 trading days before stabilizing the last couple of days.

Granted, in a short-time period, that is a lot of volatility with which to deal from a psychological standpoint, but the gold and silver asset price game has always been a game of psychological warfare in the eyes of fiat-currency advocating bankers. That is why raids in gold and silver prices often are executed rapidly and a rollercoaster pattern of up and down in prices often are manufactured over short-periods of time, as bankers design these raids to prevent people from seeing the forest from the trees. However, if we step back from the trees and zoom out, so we are indeed able to see the forest, a number of banker-spread narratives about US stock markets and gold are quickly destroyed and readily evident. If we observe a longer period of time since 2001, it is readily apparent, even at today’s prices, that gold’s cumulative yield has absolutely smashed the cumulative yield of the US stock market S&P500, even though with the heavily pushed agenda of the banking industry, Wall Street, and politicians, one may believe that the yield of the S&P500 has smashed the performance of gold. As you can see, from 2001, even with the recent price raid, gold has risen 390%, nearly beating the 81% yield of the S&P500 by five times.

Furthermore, though the narrative that gold is extremely risky to hold because its price is so volatile and stock markets are much safer because they rise every year is always sold to the public, by observing the above chart, we can easily spot the opposing truth to this false narrative about “gold is risky” and “stocks are safe”. During the last 16 years, the S&P500 suffered 3 bad years of performance while gold only suffered 2 bad years of performance. Furthermore, the bad years of performance for the S&P500 were much more volatile to the downside than the bad years of performance for gold, with the worst one-year performance of the S&P500 clocking in at -39% and the worst performance of gold 11% better at -28%. Though many of you may see the obvious price plunge of gold in the above chart that happened in 2008 and wonder why I did not include 2008 as a poor performing year for gold, this is because less apparent from the above chart, is the actual positive return of gold that year from the measuring period of 2 January 2008 to 2 January 2009.

Finally, gold performed much better over the above time period if denominated in numerous other global currencies other than the USD, and physical gold (especially bullion coins) also performed much better than paper gold prices as represented in the above chart. Thu,s in reality, if you compare the price of physical gold (in currencies other than the USD) to the performance of the US S&P500 stock index, the gold price has exhibited far less volatility to the downside than US stocks and even greater overall cumulative yields than the already wide gap presented above. So, had you bought physical gold during any of the years of the above time period, the only way you could have been really hurt was by first purchasing gold at the absolute peak at the end of 2011 after annoying 10-consecutive years of significant price increases, which would been hard to do even if one was choosing a random year between 2001 and 2016 to buy gold by throwing darts at a dartboard papered with the different years of this time period. In other words, for the many that truly understand the real narrative of reasons to purchase physical gold as opposed to the false narrative promoted by bankers, it is highly likely that every single one of you are still sitting on substantial gains on your physical gold stack today.

If we want a true definition of risky, consider that despite the wide support of Central Banks all over the world, including the Bank of Switzerland, the S&P500 was still only able to manage a yield of 81% over 16 years versus gold’s yield of nearly five times as much of 390%, despite the fact that gold prices are periodically dumped by bankers every year in gold futures markets by flooding these markets with billions of notional amounts of gold futures in condensed time periods sometimes as concentrated as just five to ten minutes. Even worse, as of 9 May, only 10 stocks (AAPL, AMZN, FB, MSFT, GOOGL, PM, V, HD, ORCL, and AVGO) out of the 500 that comprise the S&P500 index account for 46%, or nearly half of all gains of the S&P500 as of that date, while the situation is unbelievably even riskier in the US technology stock index, the NASDAQ. In this index, incredibly only 5 stocks (AAPL, AMZN, FB, MSFT and GOOG) out of the 2,500 stocks that comprise the NASDAQ account for nearly half of all gains as of the end of April.

Yet, the banking industry wants us to believe that a condition in which the performance of a 500 stock index largely relies of the performance of just 10 stocks, and the performance of a 2,500 stock index largely relies on the performance of just 5 stocks, is “safe”, while the physical gold market is dangerous. So let’s return to the charts above. Had one bought physical gold at the start of 2001, 2002, 2003, 2004, 2005, 2006, 2007, 2008, 2009 and 2010, one would still be sitting on decent to very significant profits as of today. And had one bought gold in 2014, 2015, and 2016, one would still be sitting on small to significant profits today. In other words, in the past 16 years, had one purchased gold at the start of 13, or 81% of these 16 years, one would still be sitting on a gain today. Risky indeed! If these statistics surprise you, it is merely because the mainstream media constantly focuses on short-time spans in which gold and silver prices drop and almost never report on longer-term trends when it comes to gold and silver. On the opposite side of this equation, the mainstream media always constantly focuses on short-term trends of US stock markets at the latter end of this massive bubble, and not the overall lackadaisical long-term performance of the US stock market.

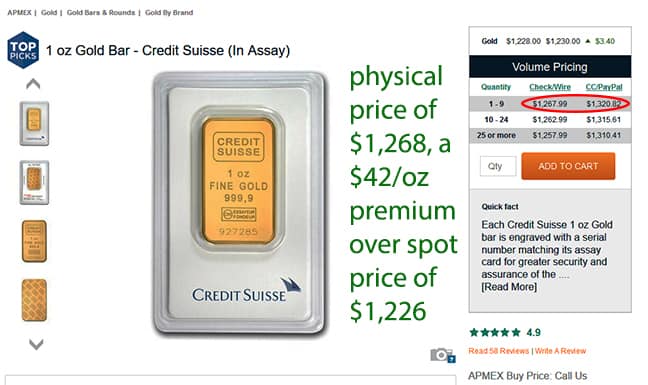

Furthermore, since gold price short-term peaked on 17 April, and then reversed downward on the back of massive billions of notional amounts of gold futures sold into paper markets, the spreads between paper and physical gold have grown larger at a time when spreads should be falling, if the downward slide in gold prices were indeed occurring within the parameters of free market forces. On 17 April, a 1-oz Credit Suisse gold bar sold at a $33 an ounce premium over spot, and today, as I write this, that same 1-oz Credit Suisse gold bar is selling at a $42 an ounce premium over spot. So we must ask ourselves, “Why is the premium of physical gold over paper gold prices growing as gold prices have been dropping?” Of course, if you’ve been following my articles for a while now, the answer is very simple to extract.

So just as I warned earlier in early March repeatedly on my SKWealthAcademy Snapchat channel that everyone should be hedging against potential big drops in gold and silver asset prices, now that many PM stocks have retreated all the way back to their March price lows, the question is why so few see this as a buying opportunity, while constantly heeding Wall Street’s “buy the dip” plea every time US stocks pull back in price. Again, the psychological games played by the banking cartel in manufacturing a roller-coaster ride in the prices of gold and silver assets obviously plays a large role in people’s wariness of gold and silver. Many have resigned themselves to the false belief that the banking cartel is all powerful and can prevent gold and silver prices from reaching and surpassing their 2008 highs ever again. A quick look at the above gold chart should squash this myth permanently, as if this were the case, gold would have steadily fallen in price since 2001 and would now perhaps be selling for $100 an ounce today instead of $1,226.

Furthermore, I’m speculating that this false belief also originates from a lack of understanding of how the 100% settle-in-physical-gold-only Shanghai gold futures markets is transforming the global banking paper gold game and stripping power from the London and New York gold traders in their ability to sustain depressed gold prices for a long period of time once they have successfully engineered a drop in gold prices (more about this topic coming soon in a future post here, so be sure to bookmark this site). Of course, most will ask the following very fair question: “If they are transforming the paper gold price game, where is the evidence, and why have gold prices been weak as of recent times, and not soaring?” However, most that ask this question are Westerners that lack an understanding of Asian culture and not only the willingness of the Chinese to make this transformation as a slow burn versus a rapid spike, but the desire of the Chinese to avoid major disruptive and dislocative events in their own economy, which a rapid $1,000 increase in the price of gold would engender.

If you understand this, and you may ask a Chinese person to explain this if you do not, this also means one should pay no attention to predictions of $10,000 gold and $500 silver this year, or even $2,000 gold and $100 silver this year, as such predictions are made every single year without bearing fruit, because honestly, there is little to no value in these speculations from the simple, logical perspective that none of us can possibly know the end price of gold and silver, nor the exact moment when and where a pillar of the global financial and monetary system will crumble that may lead to huge spikes in the price of gold and silver. Unknown and unforeseen black swan events likely will be the root of big upward spikes in the price of gold (escalation of war, collapse of a global bank, etc.), and not the transition of power in establishing gold prices from West to East, as this process will likely be a slow-burn process. This means we may still be a few years away from witnessing the Chinese State really exert any muscle in the global gold price setting process (absent of a surprise, unexpected announcement that reveals China and Russia’s true physical gold and physical silver holdings or an unexpected launch of a gold backed currency). In the meantime, understand that the upward trend in gold prices as illustrated in the above chart is extremely likely to continue, despite the white noise that happens every year with volatile roller-coaster rides in price that are designed specifically to blind us from seeing the overall picture.

Also understand that when pessimism is the highest in PM assets, that high levels of pessimism that coincide with significant drops in price very often equate to great buying opportunities that are often not seized by the general public because of the public’s concentration on the close-up view and not the bigger picture. Very often, bankers paint close-up views of gold and silver that appear highly negative and pessimistic, but in the midst of these short-term interruptions, the long-term view remains very optimistic and remains hidden from view due to a lack of mainstream media coverage of the counterbalancing optimistic view. In some cases, however, the short-term view is very pessimistic, prices have dropped tremendously, and the lower prices do not equate to value or buying opportunity. This case would describe the retail sector of America. This is because the long-term view of the US retail sector provides no counterbalancing view, as is the case with PMs, and remains negative as well. For most of this year, my social media posts consisted of warnings to assume hedges against drops in gold and silver prices. Now, with the significant drop in valuations, and a re-test of March lows, my warning is not against future drops in gold and silver prices, but rather it is a warning not to miss opportunities that have now arisen.

About the author: JS Kim is the Founder & Chief Investment Strategist of SmartKnowledgeU, a fiercely independent investment research and consulting firm with a focus on Precious Metals that is dedicated to helping people not only fight the immoral global banking cartel, but also to formulating strategies that we can implement together to help us win. Our Mission remains to fight the corrupt, criminal banking cartel and to help usher in a new renaissance of economic freedom with the re-implementation of sound money principles worldwide.

To learn more about our memberships, visit us at smartknowledgeu.com. If you have not yet subscribed to our SmartKnowledgeU YouTube channel, please subscribe today to be immediately informed of our new videos. For those that want to know more about our upcoming SKWealth Academy, you can click here to read our fact sheet.