Table of contents

Estimated reading time: 7 minutes

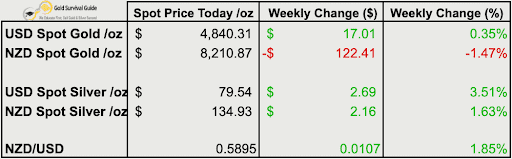

Weekly Price Overview – 15 April 2026

Precious metals were mixed this week. USD prices rose, while NZD gold fell due to a stronger Kiwi dollar. The broader trend remains intact, with short-term consolidation continuing.

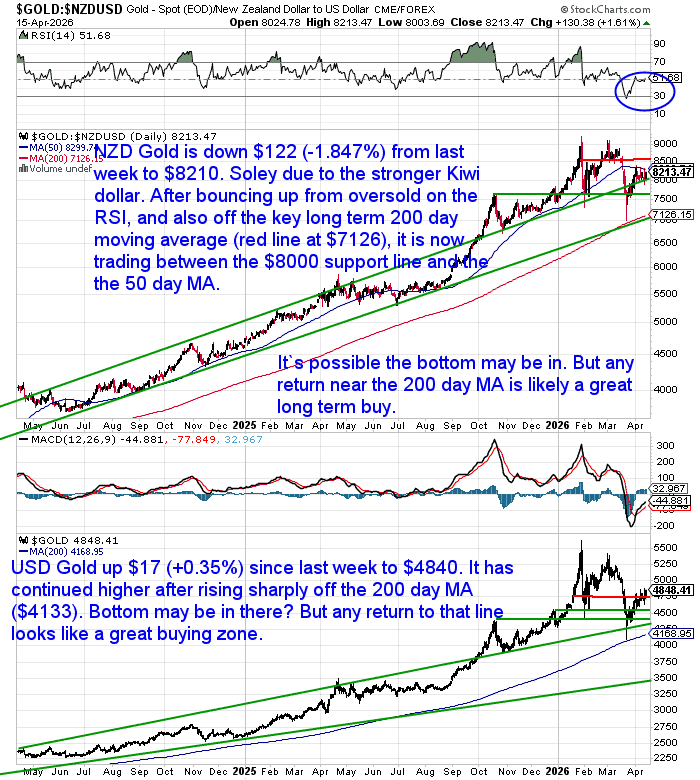

🟡 NZD gold fell $122.41 (-1.47%) to $8,210.87.

The drop was driven by a stronger NZD rather than weakness in gold. Price remains above $8,000 support and near the rising 50-day MA. The 200-day MA (around $7,126) continues to trend higher. Any pullback toward that level would likely be a solid long-term entry zone.

USD gold rose $17.01 (+0.35%) to $4,840.31.

Price continues higher after rebounding from the 200-day MA (near $4,133). The uptrend remains intact, with higher lows forming. A pullback toward the 200-day MA would still be consistent with a normal bull market move.

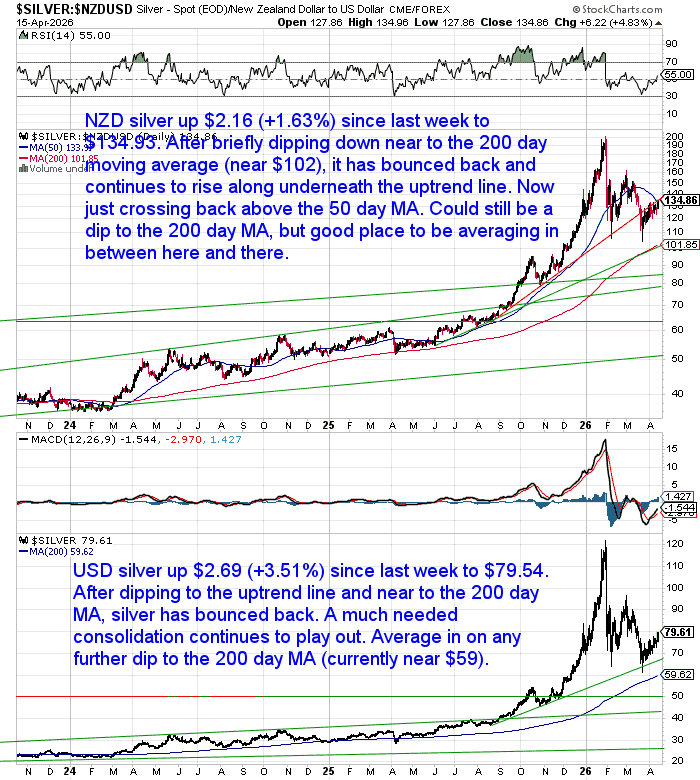

⚪ NZD silver rose $2.16 (+1.63%) to $134.93.

After dipping near the 200-day MA, silver has bounced and continues its uptrend. Price is now back above the 50-day MA. Volatility remains, but dips toward the 200-day MA may offer good averaging opportunities.

USD silver gained $2.69 (+3.51%) to $79.54.

Price has rebounded from the uptrend line and remains above the 200-day MA (near $59). Consolidation continues following the earlier rally. The broader trend remains higher.

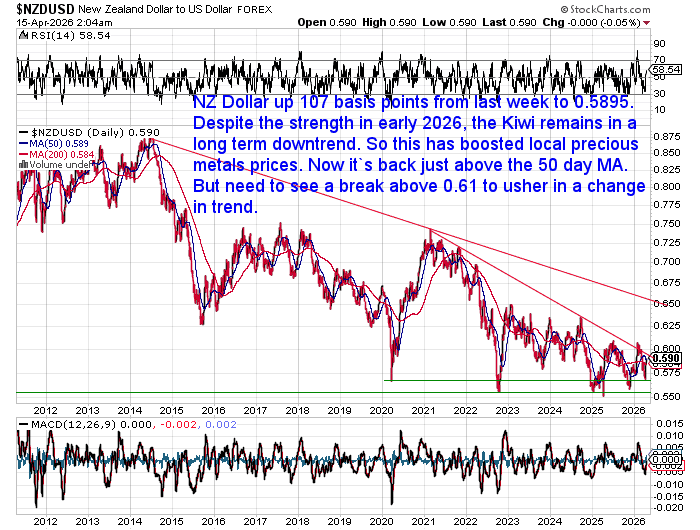

💱 NZD/USD rose 107 basis points (+1.85%) to 0.5895.

The Kiwi has strengthened short term but remains in a broader downtrend. This move has weighed on NZD gold while supporting local silver gains. A sustained move above 0.61 would be needed to shift the longer-term trend.

East vs West: A Different Response to Gold’s Pullback

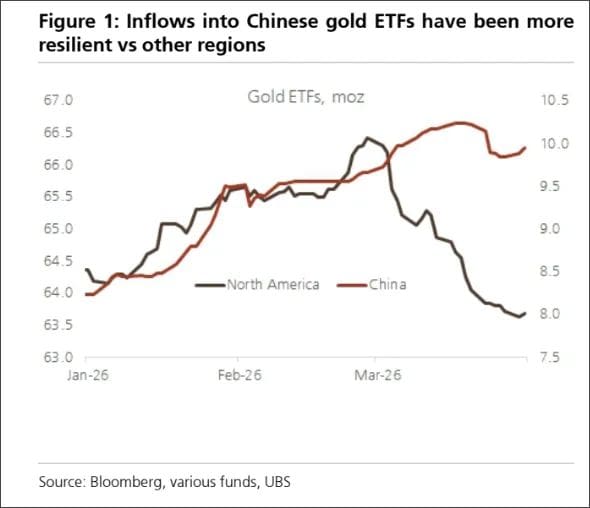

One of the more interesting signals this week isn’t the gold price… it’s who is buying and who is exiting.

During this recent correction, North American investors have been pulling money from gold ETFs, while Chinese investors have held up far better.

Source: Ronni Stoeferle

Short-Term Thinking vs Long-Term Accumulation

In the West, gold is still often treated as a trade.

When prices pull back, investors tend to reduce exposure. Positioning shifts quickly, driven by short-term price moves.

In the East, the approach is different.

Gold is seen more as long-term savings and financial insurance. So when prices dip, the response is usually to hold – or even add.

That’s exactly what we’re seeing play out.

China Isn’t Just Holding – It’s Still Buying

The actions of China’s central bank are reinforcing the same trend.

Gold reserves have now increased for 17 consecutive months, rising from 74.22 million to 74.38 million troy ounces in March.

While Western flows are often driven by sentiment and short-term positioning, Eastern demand – both public and private – appears more strategic and persistent.

USA vs NZ: The Same Stagflationary Problem, No Easy Answer

Recent US commentary points in a clear direction: stagflation risk is rising.

Data shows businesses are becoming more cautious with hiring, even as demand in parts of the economy remains strong.

As Tavi Costa put it:

“Now imagine being forced to cut rates as inflation reaccelerates.”

That’s the dilemma.

Central banks are being pulled in two directions at once:

- Weak growth calls for lower rates

- Higher inflation calls for higher rates

You can’t easily do both.

As Tavi Costa put it:

“Now imagine being forced to cut rates as inflation reaccelerates.”

That’s the dilemma.

Central banks are being pulled in two directions at once:

- Weak growth calls for lower rates

- Higher inflation calls for higher rates

You can’t easily do both.

New Zealand: The Same Dilemma Playing Out

Here in New Zealand, we’re facing a very similar backdrop.

Many businesses are still under pressure. Recent reports show a large number are operating in survival mode, with global tensions adding further strain to costs and confidence.

At the same time, inflation risks are building again, particularly with ongoing tensions in the Middle East.

That’s leading to a split in expectations:

- ANZ is now forecasting rate hikes as early as July

- Kiwibank is pushing back, warning that further hikes could be reckless and risk another recession

- Instead they favour a “wait and see” approach

A Harder Problem Than 1980

What makes this environment more difficult is the starting point.

In the early 1980s, central banks could raise rates aggressively to bring inflation under control.

Today, that option is far more limited.

Debt levels, both public and private, are significantly higher. That means higher rates have a much larger impact on households, businesses, and governments.

At the same time, cutting rates risks adding fuel to inflation.

So the challenge is greater now:

- Raise rates, and you risk breaking something

- Cut rates, and you risk reigniting inflation

There’s no easy path through it.

Chart of the Week: Is Your Wealth Actually Growing?

Source: Jacob Wright

At first glance the chart looks busy, but the message is simple.

- Green line: The buying power of the US dollar — steadily falling since 1913

- Black line: Global money supply — rising as more currency is created

- Purple line: The S&P 500 priced in US dollars — appears to be going up

- Gold line: The S&P 500 priced in gold — a very different story

What It’s Showing

Over time, more currency is created.

As that happens, each unit of currency buys less.

That’s why the stock market can appear to rise strongly in dollar terms… while delivering a very different result when measured against gold.

In fact, when priced in gold, the S&P 500 peaked back in 2000 and has struggled to make new highs since.

The Bigger Picture

Step back, and a clearer picture forms.

In the West, markets are still largely approached through a short-term, price-based lens.

But underneath that, something more important is happening:

- Central banks are constrained

- Inflation pressures are building again

- And the purchasing power of currency continues to decline over time

This is the environment those decisions are being made in.

While one group reacts to price… another continues to accumulate real assets steadily, regardless of short-term moves.

Because in the end, it’s not just about whether an asset goes up in price.

It’s about whether it holds its value in real terms.

If you want help acquiring assets that hold their value in real terms, get in touch.

Glenn's dedication to educating individuals on wealth protection through precious metals has helped over 2400 clients from New Zealand, Australia, USA and Europe to safeguard their financial futures. Passionate about financial independence and lifestyle freedom, Glenn’s mission is to empower others with the knowledge and tools to thrive in today’s volatile economic environment. When he's not advising on precious metals, Glenn enjoys spending time with his family and pursuing outdoor adventures.

Education: University of Auckland Bachelor of Science

Linkedin: https://www.linkedin.com/in/glenn-thomas-0984a4310/

- Why You Should Become Your Own Central Bank - June 28, 2026

- John Butler, Josh Phair And The Case For Gradual Monetary Change - June 24, 2026

- What Could A Global Currency Reset Mean For New Zealand? - June 19, 2026