Table of contents

- Weekly Price Overview – 25 March 2026

- Higher Inflation. Lower Growth. The Word Nobody Wants to Say

- Oil Shock Playbook: Inflation Rarely Stops at the First Spike

- The Policy Trap: Debt Levels Change Everything

- Gold’s Worst Week in Decades — And Why That May Be Normal

- A Competing View: Is Gold Pricing in a Policy Mistake?

- After the Guns Fall Silent: War’s Economic Shadow

- First Signs of Stabilisation — But Not a Trend Yet

Estimated reading time: 8 minutes

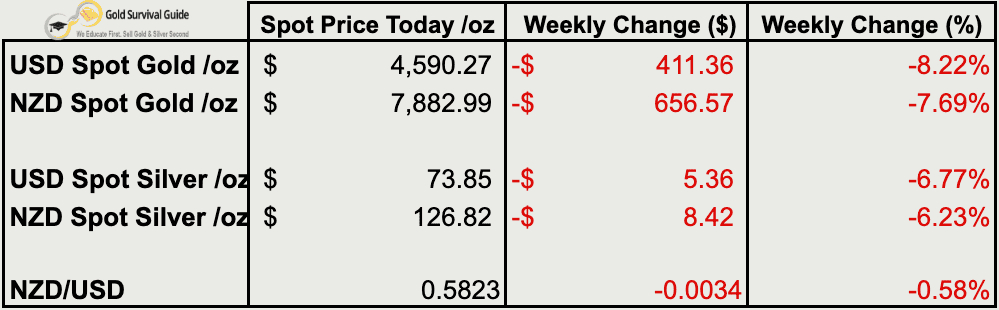

Weekly Price Overview – 25 March 2026

Precious metals corrected sharply this week as markets reacted to geopolitical tensions, shifting interest rate expectations and a firmer US dollar. Gold tested major long-term support while silver showed larger swings typical of its higher volatility, with currency moves again influencing local New Zealand prices.

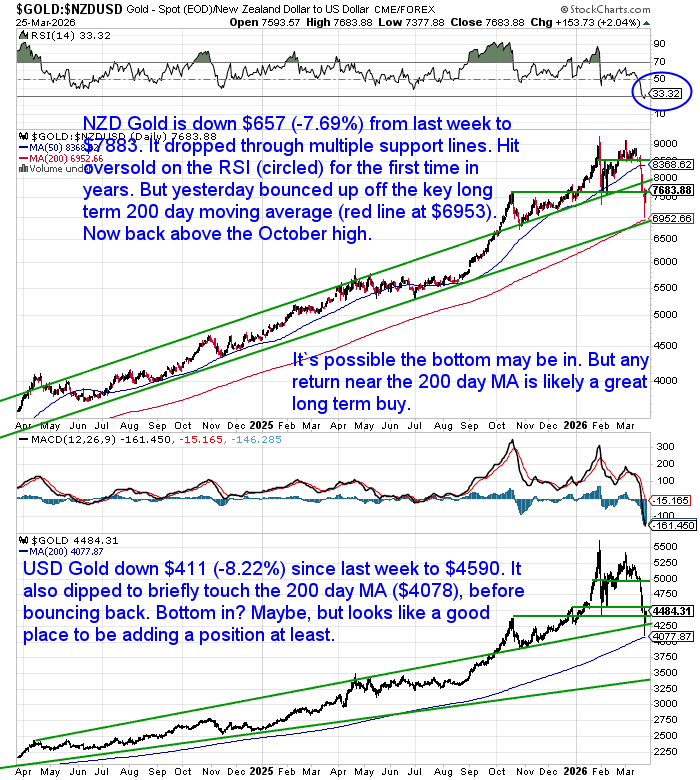

🟡 NZD gold fell $656.57 (-7.69%) to $7,882.99. Price broke through several short-term support levels and became technically oversold, with RSI reaching multi-year lows. Gold briefly tested the rising 200-day moving average near $6,953 before bouncing. Despite the sharp fall, price remains above the longer-term uptrend channel and October breakout highs. A move back toward the 200-day moving average would likely offer a constructive long-term accumulation zone.

USD gold declined $411.36 (-8.22%) to $4,590.27. The pullback briefly saw price test the rising 200-day moving average near $4,078 before recovering. Although the move was large, corrections of this size are not unusual after strong rallies. The broader structural uptrend remains intact. Further consolidation or retests of major moving averages would be normal as the market digests earlier gains.

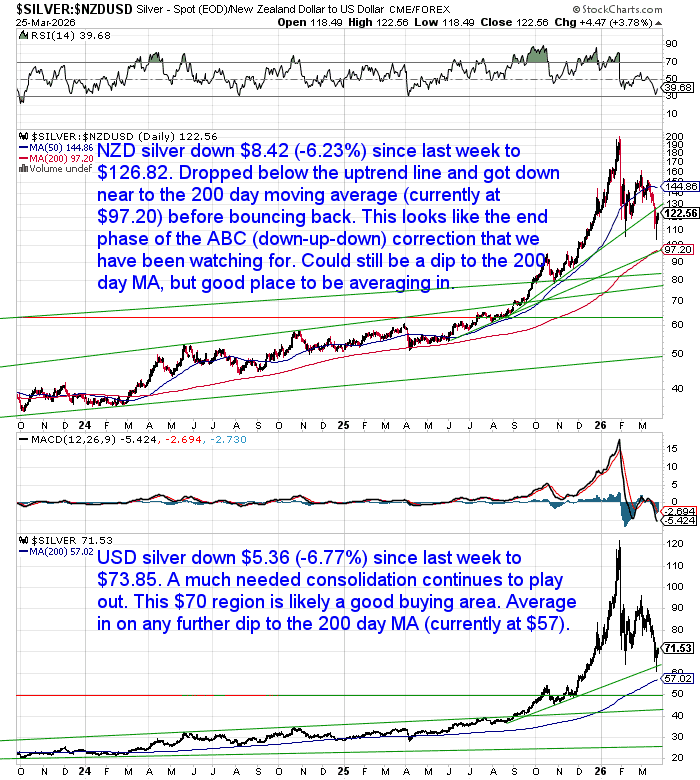

⚪ NZD silver dropped $8.42 (-6.23%) to $126.82. Silver broke below its shorter-term uptrend line and moved toward the rising 200-day moving average (currently near $97) before stabilising. The pattern still resembles a classic ABC correction after the earlier surge. Silver’s tendency to overshoot in both directions suggests choppy conditions may persist. Deeper pullbacks toward major moving averages may offer opportunities to average in.

USD silver fell $5.36 (-6.77%) to $73.85. Consolidation continues after the strong rally earlier this year. The $70 region is emerging as an important support zone based on prior price structure. Pullbacks toward the 200-day moving average (near $57) would be normal within a broader bull market and may offer attractive long-term entry points.

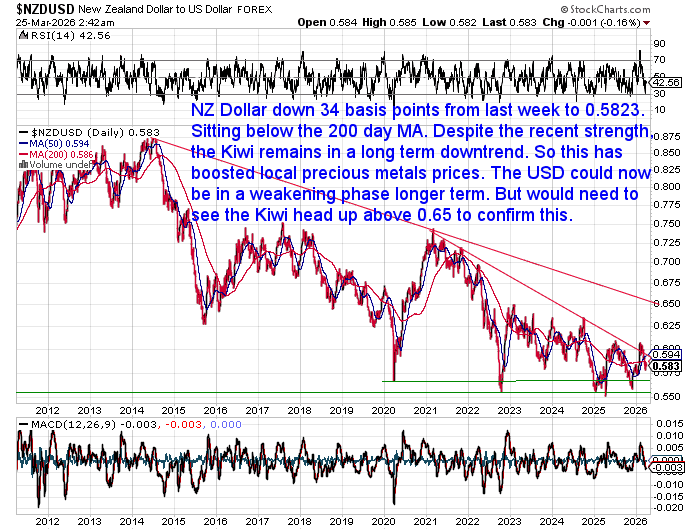

💱 NZD/USD slipped 34 basis points (-0.58%) to 0.5823. The Kiwi dollar remains below its 200-day moving average within a longer-term downtrend. Despite short-term rebounds, a sustained move above 0.65 would likely be needed to signal a meaningful trend shift. Ongoing currency weakness continues to support precious metals priced in New Zealand dollars.

📈 Takeaway: Precious metals have seen a sharp but technically understandable correction after strong advances. Gold has tested major long-term support while silver continues to show larger swings as it consolidates earlier gains. At this stage, the move still looks like a normal bull-market correction rather than a structural trend reversal, with long-term uptrends broadly intact.

Higher Inflation. Lower Growth. The Word Nobody Wants to Say

Here at home, the latest commentary from the Reserve Bank has confirmed something important — even if it wasn’t stated directly.

New Zealand is now facing higher inflation in the near term and weaker economic growth.

That combination has a name. It’s not a term central bankers like to use. And the RBNZ governor didn’t state it. But it is:

Stagflation.

The cause is clear. Oil disruption linked to conflict in the Middle East is pushing up costs across transport, food, and energy. At the same time, demand is likely to weaken.

BNZ economist Jason Wong noted that investors are increasingly worried about a prolonged war adding to inflation pressures and forcing tighter monetary policy (i.e. higher interest rates).

But Jarrod Kerr, chief economist at Kiwibank, pushed back against this idea.

His view is that rate hikes may actually not be feasible in the face of a severe demand shock hitting the Kiwi economy.

This disagreement is not trivial.

It reflects a deeper uncertainty about how central banks can respond when inflation rises for supply reasons, not because economies are overheating.

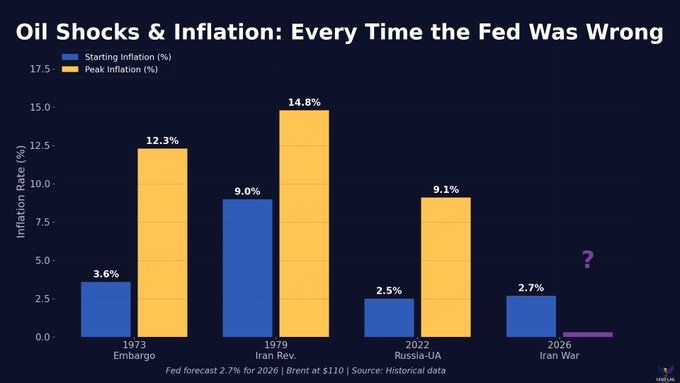

Oil Shock Playbook: Inflation Rarely Stops at the First Spike

History shows that oil shocks tend to behave in patterns.

They don’t just create a single inflation spike.

They often trigger secondary waves.

Macro analyst Tavi Costa shared a chart from portfolio manager Michael A. Gayed.

Each major oil shock — 1973, 1979, 2022 — produced a surge in inflation that policymakers initially underestimated.

Markets tend to assume central banks will respond decisively.

But they often respond late — or in the wrong direction.

This is not a one-week or even one month story. It’s much more likely to be a long term adjustment.

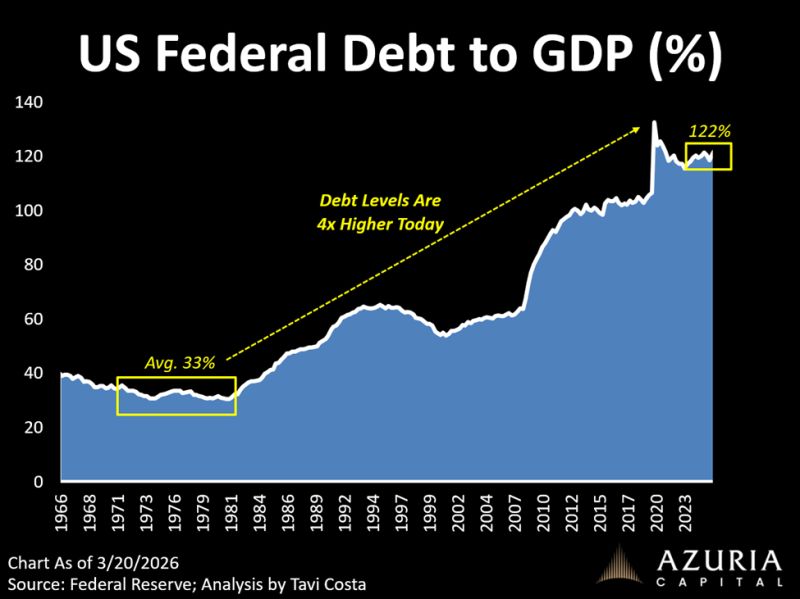

The Policy Trap: Debt Levels Change Everything

There is another reason this cycle may be different.

Government debt levels are dramatically higher than in previous inflationary periods.

Costa points out something that markets may still be underestimating.

In past inflation cycles, central banks had room to push interest rates into double digits if necessary.

Debt levels were low enough to absorb the shock.

Today, interest payments themselves are becoming a significant burden.

As a result, aggressive tightening risks destabilising government finances, banking systems and housing markets simultaneously.

Gold’s Worst Week in Decades — And Why That May Be Normal

Against this backdrop, many investors were surprised to see gold and silver fall sharply.

One prominent headline declared:

“Gold was the hottest investment in the world. Now the party is over.”

It makes for a dramatic story. But it is most likely a misleading one.

According to Ronni Stoeferle and the team behind the Sound Money Report, sharp declines in gold during crises are not unusual.

They are often linked to liquidity events.

When markets experience sudden stress, investors sell what they can sell — not necessarily what they want to sell.

Gold is one of the most liquid assets in the world.

That makes it a natural source of cash during margin calls and portfolio rebalancing.

The World Gold Council has also noted that recent declines echo risk-off episodes seen during the 2008 financial crisis and the 2020 pandemic shock.

So:

- Short-term volatility does not invalidate long-term monetary drivers.

- Precious metals often lag initial crisis moves.

- Patience can be a valuable asset class at times like these.

A Competing View: Is Gold Pricing in a Policy Mistake?

Tavi Costa offers an alternative view.

Rather than simply reflecting forced liquidation, he suggests gold’s weakness may indicate markets are pricing in tighter monetary policy ahead.

If investors believe central banks will respond aggressively to renewed inflation, real interest rate expectations can rise — pressuring gold in the short term.

But Costa questions whether such tightening is actually sustainable in today’s debt-heavy world. (Much like the view of Kiwibank economist Jarod Kerr that we shared earlier).

After the Guns Fall Silent: War’s Economic Shadow

Eventually, all conflicts end. But their economic consequences rarely do.

Strategist John Butler points out that even after hostilities cease, structural changes often remain.

- Shipping costs can stay elevated.

- Insurance premiums rise.

- Energy logistics become permanently more expensive.

These shifts feed through into food prices, manufacturing costs and ultimately consumer prices.

Investor implications

- Inflation persistence risk increases after major geopolitical disruptions.

- It pays to look beyond immediate headlines. But rather at the longer term more permanent effects.

First Signs of Stabilisation — But Not a Trend Yet

The last couple of days have shown gold and silver bouncing back after hitting key support levels

It’s too early to say a bottom is in, but it looks like we could be getting close.

For investors, the key lesson is not about timing the exact bottom in gold or silver.

It is about understanding why tangible assets remain relevant in a world of rising fiscal pressure, policy uncertainty and geopolitical tension.

Physical precious metals carry no counterparty risk. They are not dependent on a promise to pay.

Right now looks like a very good entry point. And unlike a couple of months ago hardly anyone in the public is buying.

If you would like to review your current precious metals allocation — or simply understand your options — our team is here to help.

You can request a quote, discuss secure storage solutions, or just ask questions.

Glenn's dedication to educating individuals on wealth protection through precious metals has helped over 2400 clients from New Zealand, Australia, USA and Europe to safeguard their financial futures. Passionate about financial independence and lifestyle freedom, Glenn’s mission is to empower others with the knowledge and tools to thrive in today’s volatile economic environment. When he's not advising on precious metals, Glenn enjoys spending time with his family and pursuing outdoor adventures.

Education: University of Auckland Bachelor of Science

Linkedin: https://www.linkedin.com/in/glenn-thomas-0984a4310/