Table of contents

Estimated reading time: 7 minutes

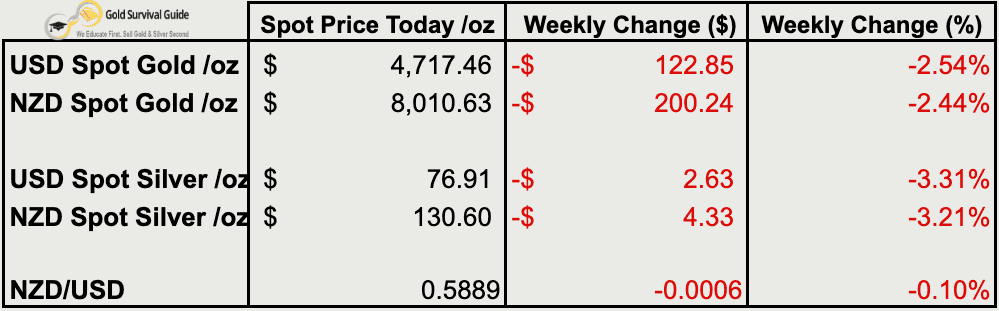

Weekly Price Overview – 22 April 2026

Precious metals pulled back this week, with both USD and NZD prices lower. The broader uptrend remains intact, but short-term consolidation is continuing after recent highs.

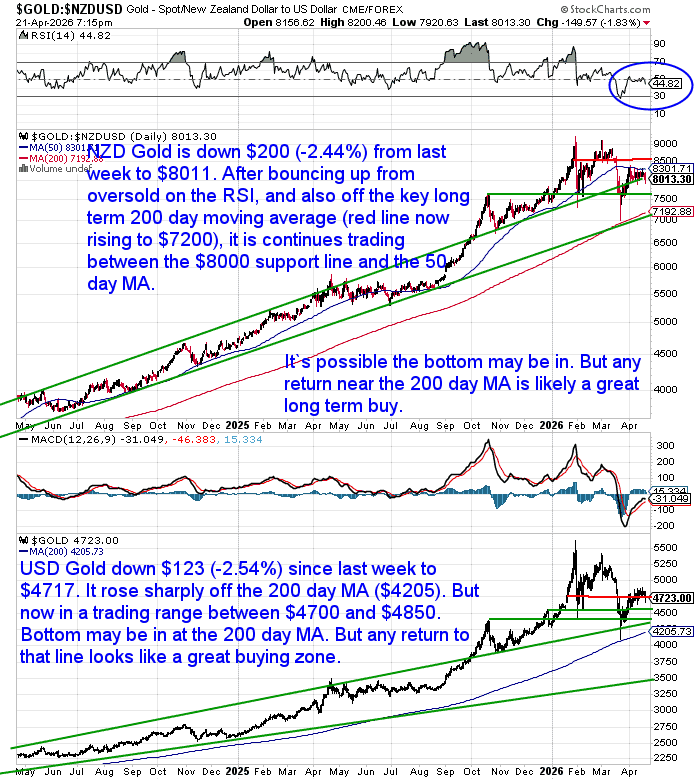

🟡 NZD gold fell $200.24 (-2.44%) to $8,010.63.

The move was mainly driven by a softer USD gold price, with the Kiwi dollar little changed and not a major factor this week. Price is holding above key $8,000 support and near the 50-day MA. The 200-day MA (around $7,200) continues to trend higher. Any pullback toward that level would likely offer a strong long-term entry.

USD gold dropped $122.85 (-2.54%) to $4,717.46.

After rebounding from the 200-day MA (near $4,205), gold is now consolidating between $4,700 and $4,850. The broader trend remains upward, with the 200-day MA acting as key long-term support.

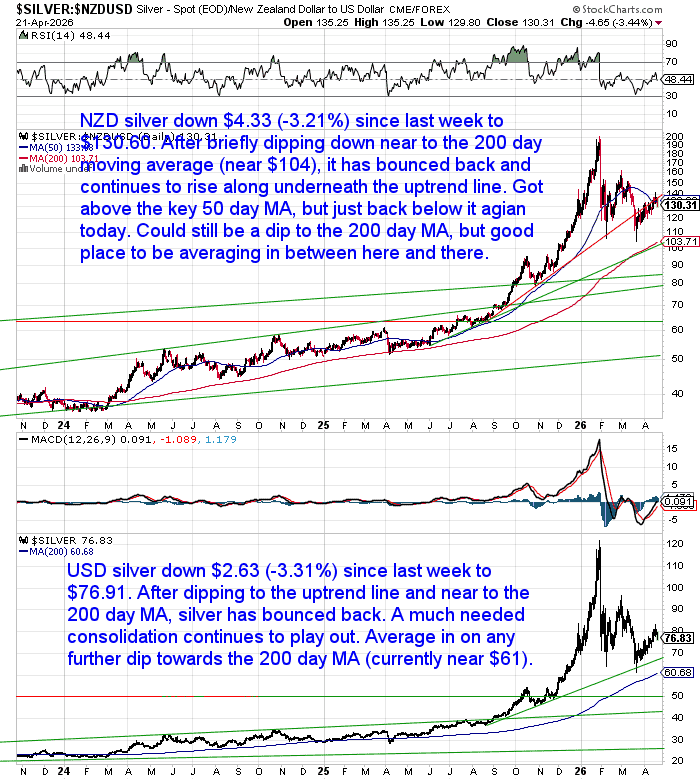

⚪ NZD silver fell $4.33 (-3.21%) to $130.60.

Silver dipped back below the 50-day MA after a recent bounce. The uptrend remains intact, but volatility is high. A move back toward the 200-day MA (near $104) could offer good averaging opportunities.

USD silver declined $2.63 (-3.31%) to $76.91.

Price has pulled back after testing higher levels but remains above the long-term uptrend and the 200-day MA (near $61). Consolidation continues following the strong rally.

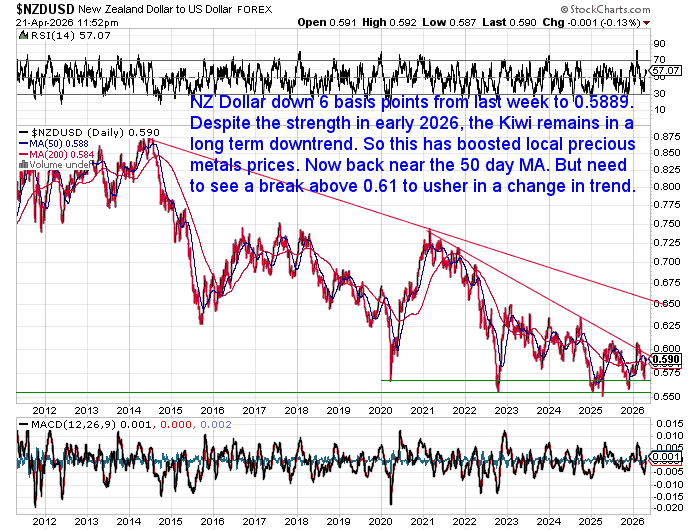

💱 NZD/USD slipped 6 basis points (-0.10%) to 0.5889.

The Kiwi remains in a broader downtrend despite recent strength earlier this year. This continues to support NZD precious metals prices. A sustained break above 0.61 would be needed to signal a trend shift.

Silver Survey 2026: Smaller Deficit, Same Underlying Tightness

This week’s 2026 World Silver Survey gives us a clearer picture of what’s actually changing in the silver market.

Yes, the headline number is softer, with the supply deficit is expected to shrink to around 76 million ounces in 2026. Down from a much larger ~318 million ounces in 2025.

But the reason why matters.

The drop is being driven mainly by weaker investment demand via Exchange Traded Products (ETPs). Last year saw very strong inflows (~278Moz). This year, that is expected to fall sharply (closer to ~30Moz), with outflows already showing up in Q1.

So the deficit is smaller — not because supply has surged, but because investment flows have cooled.

Looking at the survey data, physical demand has held up better than you might expect. Retail coin demand improved over the past year, and positioning has been reduced. That leaves the market less crowded and gives room for new buying to come in.

But in the very short term, we are starting to see some softening in retail demand — particularly here in New Zealand this month.

Short-term demand can move around, but the underlying structure changes much more slowly.

So there’s a difference between the underlying trend (still supportive) and the current pause (short-term weakness).

What’s Supporting Silver Right Now

Ronni Stoeferle this week discussed how silver remains in a different position to gold.

It is still relatively affordable, especially for investors who feel priced out of gold at current levels.

But more importantly, it is a much smaller market.

That means even modest shifts in demand can move the price quickly.

At the same time, industrial demand continues to build. Solar, defence, and electronics all rely on silver. That demand is steady and structural.

So when investment demand returns – even in a smaller way – it meets a market that is already tight.

That combination is what can drive sharp moves.

From a cycle point of view, this still looks early. We are not yet seeing broad leadership from the junior mining sector, which is often a later-stage signal.

East vs West – Now Showing Up in Silver

We’re also seeing a similar pattern to what we reported on in gold last week, emerge in silver.

Here in New Zealand, as already noted, retail demand has softened. Premiums on silver bars and coins have been falling. In some cases, such as Mint Boxes of Silver Maples, they are the lowest we’ve seen in quite a while.

So local and western demand is quieter right now.

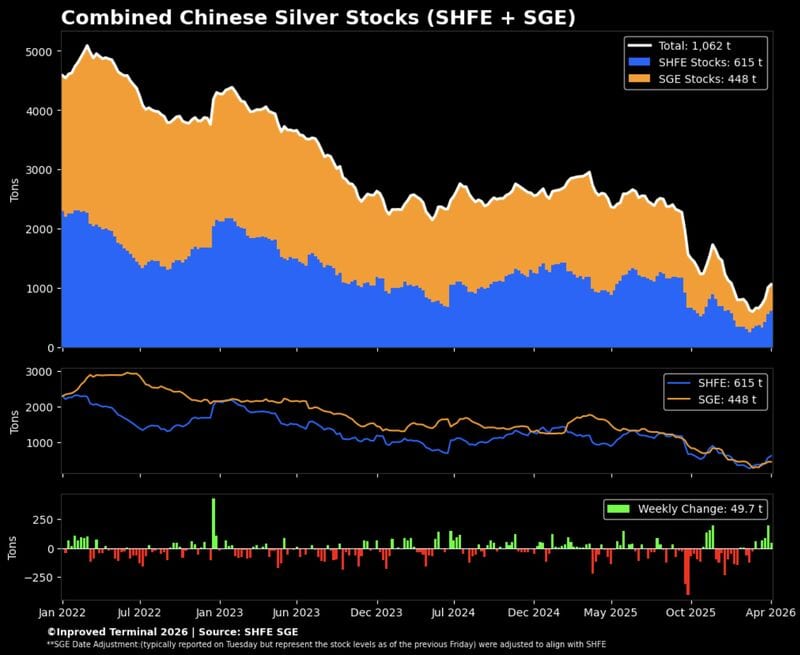

But in China and Hong Kong, the picture is different.

Chinese silver inventories have recently risen to a 3-month high, with combined stocks on the SHFE and SGE moving above 1,000 tonnes. (Source: Hugo Pascal)

This may reflect restocking or tightening supply conditions.

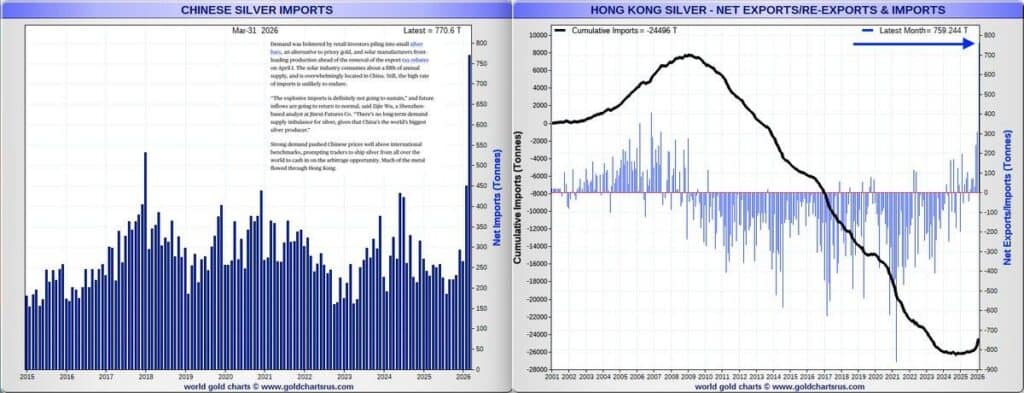

Now add this:

Import data through China and Hong Kong has been strong.

Source: James Anderson

Physical metal is still flowing into the region, where demand remains firm.

The Simple Silver Takeaway

Nothing here points to a breakdown in silver demand.

Instead, we’re seeing a shift in who is buying.

Western investment flows have cooled for now. But physical demand – particularly in China and across Asia – remains solid. Like we reported on gold last week, the east are masters at buying price dips.

And in a small market like silver, that matters.

Because when investment demand returns, it won’t be meeting a surplus.

It will be meeting a market that is still in deficit.

What This Means for Gold and Silver

There’s still a lot of noise in the market right now.

Geopolitics, oil, interest rates — the headlines are shifting daily.

But stepping back, the role of precious metals becomes clearer.

Gold isn’t there to outperform everything else. It’s there to balance a portfolio. When markets become unstable, it has a long track record of reducing volatility and smoothing out the ride.

Even a small allocation can make a difference.

And if conditions deteriorate further, gold has consistently held its value on the other side.

Silver sits slightly differently.

We’re now into the sixth straight year of supply deficits. Mine supply has been flat to falling for years, while industrial demand continues to grow across solar, electronics, and emerging technologies.

At the same time, above-ground stockpiles are being drawn down.

The margin for error is shrinking. It doesn’t take a large shift in investment demand to tighten the market further.

So while short-term demand can move around, the longer-term setup remains in place.

What To Do From Here

This is where a steady approach pays off.

Not trying to pick the exact bottom. Not reacting to every headline.

But building a position over time, while the underlying conditions remain supportive.

If you’re looking to add to your gold or silver holdings — or just want to talk through the current setup — feel free to get in touch.

We’re here to help you make sense of it and take the next step with confidence.

Glenn's dedication to educating individuals on wealth protection through precious metals has helped over 2400 clients from New Zealand, Australia, USA and Europe to safeguard their financial futures. Passionate about financial independence and lifestyle freedom, Glenn’s mission is to empower others with the knowledge and tools to thrive in today’s volatile economic environment. When he's not advising on precious metals, Glenn enjoys spending time with his family and pursuing outdoor adventures.

Education: University of Auckland Bachelor of Science

Linkedin: https://www.linkedin.com/in/glenn-thomas-0984a4310/