New Zealand currently holds zero official gold reserves.

Unlike most central banks around the world, the Reserve Bank of New Zealand (RBNZ) does not own any gold as part of its official reserve assets. In fact, New Zealand has not held any gold reserves since 1991, when the Reserve Bank sold its remaining holdings.

That makes New Zealand unusual.

Over the past decade, central banks around the world have been buying gold at the fastest pace in decades. Countries such as China, India, Turkey and Poland have all increased their gold holdings as geopolitical tensions, inflation concerns and questions about the international monetary system have grown.

So why does New Zealand hold no gold at all?

And if central banks around the world are accumulating gold, should New Zealand reconsider its position?

These questions have become more relevant as gold has reached record highs and central bank demand has surged. We’ve even had readers ask whether New Zealand could simply create money and buy gold reserves given the country currently has none.

This article examines how much gold New Zealand has, why the Reserve Bank sold its gold reserves, how New Zealand compares with other countries, and whether there is a case for New Zealand to hold gold again in the future.

Quick Answer

The Reserve Bank of New Zealand currently holds zero gold reserves.

New Zealand sold its remaining gold reserves in 1991 and now holds foreign currencies, government securities and other highly liquid reserve assets instead.

While many central banks have increased their gold holdings in recent years, the RBNZ has repeatedly stated that gold does not meet its liquidity requirements.

Table of contents

- Quick Answer

- Central Banks Have Changed Their View On Gold

- Why Are Central Banks Buying Gold Again?

- How Much Gold Does The Reserve Bank Of New Zealand Have?

- When Did New Zealand Sell Its Gold Reserves?

- Why Did New Zealand Sell Its Gold?

- How Does New Zealand Compare With Other Countries?

- Will Central Banks Continue Buying Gold?

- Why The Reserve Bank Is Unlikely To Buy Gold

- Was Selling The Gold The Right Decision?

- Should New Zealand Buy Gold Again?

- Why Doesn’t New Zealand Simply Print Money And Buy Gold?

- Conclusion: The World Is Buying Gold. New Zealand Holds None.

- Frequently Asked Questions About New Zealand’s Gold Reserves

Central Banks Have Changed Their View On Gold

One reason New Zealanders increasingly ask about the country’s gold reserves is because central banks themselves have dramatically changed their attitude towards gold over the past two decades.

During the 1990s and early 2000s, many central banks viewed gold as an outdated reserve asset. Countries regularly sold hundreds of tonnes of gold each year and increased their holdings of government bonds and foreign currencies instead.

Following the 2008 Global Financial Crisis, however, attitudes began to change. Central banks collectively switched from being net sellers of gold to net buyers.

The trend accelerated further after Russia’s foreign exchange reserves were frozen following its invasion of Ukraine in 2022. Since then, central bank gold purchases have reached record levels as countries increasingly seek reserve assets that carry no counterparty risk and cannot be frozen or controlled by another nation.

The chart below illustrates this change.

From 1995 to 2009, central banks were net sellers of gold. In some years they sold more than 600 tonnes. Since 2010 they have been net buyers, purchasing an average of around 473 tonnes per year between 2010 and 2021.

Following the sanctions imposed on Russia in 2022, buying accelerated even further. Between 2022 and 2025, central banks purchased more than 1,000 tonnes of gold annually on average, more than double the previous decade’s average.

Why Are Central Banks Buying Gold Again?

Unlike government bonds or bank deposits, gold carries no counterparty risk. It is not dependent on the financial health of a government, central bank or financial institution. Gold cannot be printed, defaulted on or frozen by another country.

For this reason, gold has long played a role in central bank reserves, helping diversify reserve assets and acting as a form of financial insurance during periods of monetary, financial and geopolitical stress.

Several trends appear to be driving demand:

- Rising government debt levels around the world.

- Concerns about inflation and currency debasement.

- Geopolitical tensions and sanctions risk.

- A desire to reduce reliance on the US dollar.

- Growing uncertainty about the future international monetary system.

Gold is typically held alongside foreign currencies and government securities as part of a country’s reserve assets.

Against this backdrop, New Zealand’s position is unusual. While many central banks are increasing their gold holdings, the Reserve Bank of New Zealand continues to hold none.

How Much Gold Does The Reserve Bank Of New Zealand Have?

The Reserve Bank of New Zealand currently holds zero gold reserves.

Unlike most central banks, the RBNZ does not own any gold as part of its official reserve assets. Instead, the Reserve Bank primarily holds foreign currencies, government securities, Special Drawing Rights (SDRs) and other liquid reserve assets.

The table below shows the composition of New Zealand’s official reserve assets. Notice that the line item for gold is zero.

| New Zealand’s International Reserves and Foreign Currency Liquidity | |

| (Information is disclosed in NZD 000’s) | |

| I. Official reserve assets and other foreign currency assets (approximate market value) | |

| Description | Apr_24 |

| A. Official reserve assets | 31,938,329 |

| (1) Foreign currency reserves (in convertible foreign currencies) | 21,818,171 |

| (a) Securities | 13,255,304 |

| of which: issuer headquartered in reporting country but located abroad | – |

| (b) total currency and deposits with: | 8,562,867 |

| (i) other national central banks, BIS and IMF | 8,559,007 |

| (ii) banks headquartered in the reporting country | – |

| of which: located abroad | – |

| (iii) banks headquartered outside the reporting country | 3,860 |

| of which: located in the reporting country | – |

| (2) IMF reserve position | 752,432 |

| (3) SDRs | 4,832,012 |

| (4) gold (including gold deposits and, if appropriate, gold swapped) | – |

| volume in fine troy ounces | – |

| (5) other reserve assets | 4,535,714 |

| financial derivatives | (1,183,869) |

| loans to non-bank non-residents | – |

| other | 5,719,583 |

| B. Other foreign currency assets | 827,496 |

| securities not included in official reserve assets | – |

| deposits not included in official reserve assets | 1,194,499 |

| loans not included in official reserve assets | – |

| financial derivatives not included in official reserve assets | (367,003) |

| gold not included in official reserve assets | – |

| other | – |

In fact, New Zealand has not held any official gold reserves since 1991.

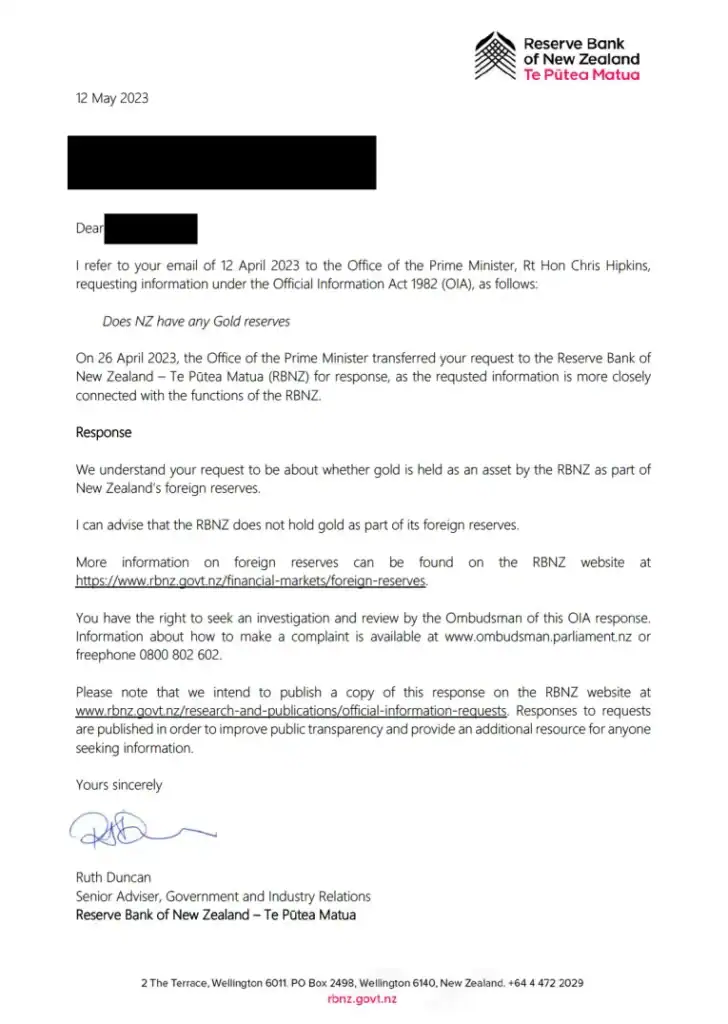

The RBNZ Confirms No Gold Reserves in Official Information Act Request

On the 12 May 2023, the RBNZ also confirmed in an Official Information Act request that:

“…the RBNZ does not hold gold as part of its foreign reserves.”

Key Fact: New Zealand Gold Reserve Snapshot

- Official gold reserves: 0 tonnes

- Last gold sold: 1991

- Confirmed by: RBNZ Official Information Act response (2023)

- Current reserve assets: Foreign currencies, government bonds and SDRs

When Did New Zealand Sell Its Gold Reserves?

Many New Zealanders assume that because the Reserve Bank holds no gold today, it never held much gold in the first place.

In fact, New Zealand once held significant gold reserves as part of its official reserve assets.

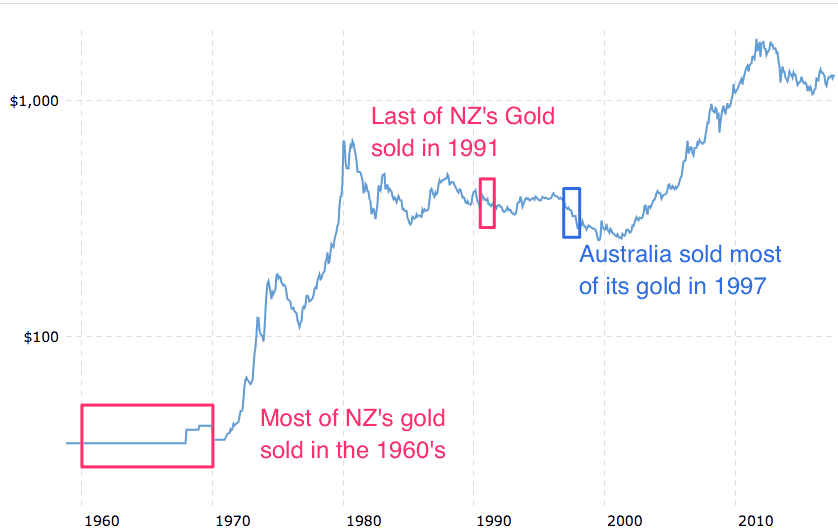

Historical IMF data suggests New Zealand’s gold reserves peaked at approximately US$35 million in 1961, equivalent to around 31 tonnes of gold at the official Bretton Woods gold price of US$35 per ounce.

Most of those reserves were sold during the 1960s, when the international monetary system was still operating under the Bretton Woods framework and the US dollar remained convertible into gold at US$35 per ounce.

The final remnants of New Zealand’s gold reserves were sold in 1991.

According to the Reserve Bank Museum:

“Most of the gold reserves were divested in the 1960s. The last remaining gold was sold in 1991.” Source.

New Zealand has now spent more than three decades with no official gold reserves.

Selling gold was not unique to New Zealand.

During the second half of the twentieth century, many central banks reduced their gold holdings as confidence in financial markets grew and reserve managers increasingly favoured foreign currencies and government securities.

However, relatively few countries chose to eliminate their gold reserves entirely.

New Zealand did.

Why Did New Zealand Sell Its Gold?

To understand why New Zealand sold its gold, it helps to think like a reserve manager rather than a gold investor.

Central banks do not primarily hold reserves to make a profit. They hold reserves to meet foreign currency needs, support financial stability and respond to periods of market stress.

From that point of view, gold came to be seen by many reserve managers as less useful than foreign currency assets.

Gold does not pay interest, while government bonds and bank deposits can generate income. As global financial markets developed, these assets became increasingly attractive to reserve managers.

Gold was also seen as less practical. If a country suddenly needs US dollars or euros, holding those currencies directly is simpler than first selling gold and converting the proceeds.

As a small trading nation, New Zealand relies on access to foreign currency to pay for imports, meet international obligations and manage periods of market stress. From a conventional reserve-management perspective, foreign currency assets were viewed as more practical than gold.

By the late twentieth century, gold was also increasingly viewed by many Western policymakers as a legacy asset from an older monetary system. Once the link between currencies and gold was broken, gold no longer played the same formal role in the international financial system.

So the Reserve Bank’s decision can be understood as part of a wider shift in thinking. Gold was seen as non-yielding, less useful for day-to-day reserve management, and no longer essential in a world of floating currencies and deep government bond markets.

However, many countries reached a different conclusion. While they reduced their gold holdings, most retained at least some gold as part of their reserves.

How Does New Zealand Compare With Other Countries?

New Zealand is not unusual because it holds less gold than major powers such as the United States, Germany or China.

New Zealand is unusual because it holds no gold at all.

Most countries retain at least some gold as part of their official reserves, even when gold represents only a small percentage of their total reserve assets.

Australia, for example, sold most of its gold in 1997 but still retains around 80 tonnes. Singapore has steadily increased its gold holdings in recent years, while many European countries continue to hold significant reserves despite no longer operating under a gold-backed monetary system.

The contrast becomes even more striking when New Zealand is compared with much smaller economies. Even countries such as Fiji and Haiti have reported small official gold holdings in recent years.

Rather than comparing New Zealand with major powers, it is more useful to compare it with smaller developed economies and regional peers.

The table below shows how New Zealand compares with a selection of countries of similar size or economic profile.

| Country | Gold Reserves (Tonnes) |

|---|---|

| Portugal | 382 |

| Singapore | 228 |

| Finland | 49 |

| Ireland | 12 |

| Australia | 80 |

| New Zealand | 0 |

Many smaller and medium-sized nations continue to regard gold as a useful reserve asset.

New Zealand remains one of a relatively small number of countries that holds no official gold reserves.

Related: Australia Has 80 Tonnes Of Gold. How Much Does New Zealand Have?

Will Central Banks Continue Buying Gold?

Nobody knows for certain whether central banks will continue buying gold at the extraordinary pace seen in recent years.

However, several factors suggest that gold is likely to remain an important reserve asset for many countries.

Central banks continue to face many of the same challenges that helped drive gold demand higher in the first place. These include rising government debt levels, geopolitical tensions, inflation concerns and a growing desire among some countries to reduce their dependence on the US dollar.

Many countries also still hold relatively modest gold allocations compared with some of the world’s largest gold holders. The United States, Germany, Italy and France hold a significant proportion of their reserves in gold, while countries such as China and India continue to hold much lower allocations despite increasing their purchases in recent years.

Taken together, these trends suggest that some countries could continue adding to their gold holdings if they choose to further diversify their reserves.

More broadly, central banks no longer appear to view gold the way they did during the 1990s and early 2000s. Back then, many policymakers regarded gold as a relic of a previous monetary era. Today, many view it as a strategic reserve asset once again.

Some countries have recently sold or mobilised part of their gold holdings when circumstances required it. Turkey, for example, reduced its gold reserves during the market volatility that followed the 2026 Iran conflict as authorities sought additional liquidity and financial stability.

Far from undermining the case for holding gold, episodes like this demonstrate one of the reasons central banks hold reserve assets in the first place. Gold can be accumulated during stable periods and drawn upon when needed.

The more important question is not whether central banks occasionally sell gold, but whether they remain net buyers over time.

For most of the period from 1995 to 2009, central banks collectively reduced their gold holdings. Since 2010 they have done the opposite.

As long as central banks continue to buy more gold than they sell, gold appears to be regaining a role within the international monetary system that many thought it had permanently lost.

Related: Why New Zealand Won’t Have Any Say in a Global Currency Reset

Why The Reserve Bank Is Unlikely To Buy Gold

Despite the surge in central bank gold buying around the world, it remains unlikely that the Reserve Bank of New Zealand will add gold to its reserves anytime soon.

One reason for this is that the Reserve Bank has consistently argued that gold does not fit the role it expects reserve assets to perform.

Back in 2012, a reader forwarded us the following response from the Reserve Bank of New Zealand:

The Reserve Bank of New Zealand has not held any gold reserves since 1991.

…The Reserve Bank is not, at this stage, planning to include gold in our foreign reserve portfolio. The Reserve Bank’s position is that gold does not meet our liquidity requirements.

The Reserve Bank is using a specific definition of liquidity.

When reserve managers talk about liquidity, they are often referring to how quickly an asset can be deployed to meet immediate foreign currency needs. Foreign exchange reserves held directly in US dollars, euros or other major currencies can be used instantly. Gold, by contrast, usually needs to be sold or pledged before it can be converted into the required currency.

From the Reserve Bank’s perspective, foreign currencies and government securities are therefore more useful for day-to-day reserve management.

This helps explain why New Zealand’s reserves are primarily held in foreign currencies, government bonds and Special Drawing Rights (SDRs), rather than gold.

Many other central banks have reached a different conclusion.

While they also hold substantial foreign currency reserves, they continue to allocate a portion of their reserves to gold. They do not necessarily view gold and foreign currency reserves as competing assets, but as complementary ones.

Whether New Zealand’s approach remains appropriate is ultimately a matter of debate.

Was Selling The Gold The Right Decision?

Whether New Zealand was right to sell its gold reserves depends largely on how one views the purpose of a country’s reserves.

Supporters of the decision would argue that the Reserve Bank acted rationally based on the information and priorities of the time.

Gold pays no interest and cannot be used directly to meet immediate foreign currency needs. For a small trading nation like New Zealand, foreign currencies and government securities were viewed as more practical reserve assets.

It is also important to avoid judging past decisions solely through the benefit of hindsight. Reserve managers in the 1960s and 1990s could not know how gold would perform over the following decades, just as today’s policymakers cannot know what gold will do over the next thirty years.

However, there is another side to the debate.

While many countries reduced their gold holdings during the second half of the twentieth century, relatively few chose to eliminate them entirely. Countries such as Australia, the United Kingdom, France, Germany and Switzerland all retained at least some gold reserves.

The reason is that gold provides something most reserve assets do not.

Unlike government bonds, bank deposits and foreign currency reserves, gold does not depend on another institution’s promise to pay. It carries no counterparty risk.

If reserves exist purely to provide immediate foreign currency liquidity, then the Reserve Bank’s preference for foreign currencies and government bonds is understandable.

However, if reserves are also intended to provide long-term monetary resilience and diversification, then the case for retaining at least some gold becomes much stronger.

Recent central bank behaviour suggests many countries are placing greater value on these characteristics than they did twenty or thirty years ago.

The debate therefore may not be whether New Zealand was right or wrong to sell its gold reserves decades ago.

The more relevant question may be whether New Zealand would make the same decision if it were starting from scratch today.

Should New Zealand Buy Gold Again?

Whether New Zealand should own gold reserves again is ultimately a question of reserve management philosophy.

Those who support the current approach would argue that New Zealand’s reserves should remain focused on assets that can be deployed immediately during a financial crisis.

Others would argue that gold still deserves a place within a diversified reserve portfolio.

Importantly, this is not an either-or decision.

Most countries that hold gold reserves also hold substantial amounts of foreign currencies and government securities. Gold is typically used alongside other reserve assets rather than as a replacement for them.

Whether New Zealand should follow that approach remains open to debate.

One suggestion often comes up:

If New Zealand has no gold reserves, why doesn’t the Reserve Bank simply create some new money and buy gold?

Why Doesn’t New Zealand Simply Print Money And Buy Gold?

One of the most interesting questions we’ve received from readers is this:

If New Zealand has no gold reserves, why doesn’t the Reserve Bank simply create new money and use it to buy gold?

At first glance, the idea appears surprisingly logical.

Imagine the Reserve Bank created NZ$10 billion and used it to purchase gold.

New Zealand would gain billions of dollars worth of gold reserves. The money would be exchanged for a real asset rather than spent directly into the economy.

Compared with printing money to fund government spending, this may appear far less inflationary.

However, there is a problem.

The Money Still Exists

When the Reserve Bank creates money to buy gold, the seller receives that money.

New Zealand now owns the gold, but the seller now owns the NZ dollars.

The transaction changes who owns the assets. It does not eliminate the newly created currency.

Those NZ dollars can then be spent, invested, exchanged for another currency or used to purchase other assets.

New Zealand has gained a gold reserve, but there are still more NZ dollars in existence than before.

What If The Gold Is Bought Overseas?

If the gold is purchased from a foreign supplier, it may seem that the newly created NZ dollars leave the country and therefore cannot contribute to inflation within New Zealand.

But foreign sellers are unlikely to want to hold large quantities of NZ dollars indefinitely.

Eventually those NZ dollars will typically be exchanged for another currency through foreign exchange markets, increasing the supply of NZ dollars relative to other currencies.

Someone, somewhere, must ultimately hold the additional NZ dollars that were created.

This means the increase in the supply of NZ dollars still exists, even if the original seller immediately exchanges them for US dollars, euros or another currency.

The Exchange Rate Matters

If New Zealand creates billions of dollars of new currency without a corresponding increase in the production of goods and services, the additional supply of NZ dollars may place downward pressure on the currency’s value.

A weaker New Zealand dollar makes imports more expensive.

Some readers might argue this is not necessarily a major problem if it mainly affects imported consumer goods. However, New Zealand also relies heavily on imported fuel, machinery, medical equipment, industrial components and many other essential goods.

If the NZ dollar falls, the cost of those imports rises as well.

Economists often refer to this as imported inflation.

But Isn’t Some Inflation Someone Else’s Problem?

A reasonable counterargument is that much of the newly created money may end up circulating overseas rather than within New Zealand itself.

There is some truth to this.

However, foreign exchange markets connect New Zealand to the rest of the world. If overseas holders attempt to exchange large amounts of NZ dollars for other currencies, the effect can still be felt through exchange rates and import prices.

The inflationary impact may not appear in exactly the same way as a domestic spending programme, but it does not simply disappear.

Does This Mean New Zealand Should Never Own Gold Reserves?

Not necessarily.

The more important distinction is between buying gold with newly created money and buying gold with existing reserve assets.

If policymakers believed New Zealand should hold some gold, a stronger argument would be to reallocate part of the country’s existing reserve portfolio.

In that scenario, New Zealand would be exchanging one reserve asset for another rather than creating entirely new money in the process.

The Real Question

The debate is therefore not really about whether New Zealand should own gold.

The more important question is how such reserves would be acquired.

Creating new money to buy gold may sound straightforward, but once exchange rates, reserve management and inflation are considered, the issue becomes far more complex than it first appears.

Conclusion: The World Is Buying Gold. New Zealand Holds None.

New Zealand currently holds zero official gold reserves.

Most of the country’s gold was sold during the 1960s, with the final holdings sold in 1991. Since then, the Reserve Bank has preferred foreign currencies, government bonds and other highly liquid reserve assets.

At the same time, the rest of the world has been moving in a different direction.

After decades of selling gold, central banks became net buyers in 2010 and have purchased record amounts since 2022. Countries as diverse as China, India, Poland, Singapore and Turkey have all increased their gold holdings, while New Zealand continues to hold none.

Whether that is the right decision remains open to debate.

Supporters of the current approach argue that foreign currency reserves are more practical and liquid. Others argue that gold still provides diversification and resilience during periods of monetary, financial or geopolitical uncertainty.

What is clear is that gold remains far more important to the international monetary system than many expected twenty years ago.

Perhaps the most interesting lesson is that while gold no longer backs modern currencies, central banks still hold thousands of tonnes of it. In an increasingly uncertain world, many continue to view gold as a strategic reserve asset worth owning.

For individual investors, that raises a question worth considering.

If central banks continue to hold gold as part of their long-term reserves, should you consider holding some as part of yours?

One way to think about precious metals ownership is to become your own central bank — holding a portion of your savings in assets that do not depend on someone else’s promise to pay.

You can view our range of gold or silver.

Frequently Asked Questions About New Zealand’s Gold Reserves

No. The Reserve Bank of New Zealand currently holds zero gold reserves. The last of New Zealand’s official gold holdings were sold in 1991.

Most of New Zealand’s gold reserves were sold during the 1960s. The final remaining gold reserves were sold in 1991.

The Reserve Bank believed foreign currencies and government bonds were more practical reserve assets than gold. Gold does not generate income and was viewed as less useful for meeting immediate foreign currency and liquidity needs.

The Reserve Bank of New Zealand holds zero tonnes of gold as part of its official reserve assets.

Yes. Most countries retain at least some gold as part of their official reserves. New Zealand is one of a relatively small number of countries that holds no official gold reserves at all.

Yes. Australia sold most of its gold reserves in 1997 but still retains approximately 80 tonnes of gold.

Central banks have increasingly purchased gold since the 2008 Global Financial Crisis. Reasons include diversification, concerns about inflation, geopolitical tensions, sanctions risk and reducing dependence on the US dollar.

Modern currencies are no longer backed by gold, but many central banks still hold gold as part of their reserves. Gold remains one of the few reserve assets that carries no counterparty risk and can help diversify a country’s reserve portfolio.

The United States, Germany, Italy and France are among the largest official gold holders in the world. Together they hold thousands of tonnes of gold as part of their national reserves. China and Russia have also increased their holdings significantly in recent decades.

Yes. The Reserve Bank could purchase gold at any time if reserve management policy changed. However, it has repeatedly stated that gold does not meet its liquidity requirements.

Creating new money to buy gold would increase the supply of New Zealand dollars. Even if the gold was purchased overseas, the additional currency could affect exchange rates and contribute to imported inflation. A more practical approach would be to exchange existing reserve assets for gold.

Yes. Although currencies are no longer backed by gold, central banks continue to hold thousands of tonnes of gold as part of their reserves. In recent years they have been buying gold at the fastest pace seen in decades.

Many gold owners view gold primarily as financial insurance rather than a traditional investment. Gold is often held to provide diversification and protection during periods of monetary, financial or geopolitical uncertainty.

In theory, yes. In practice, it is highly unlikely. Modern economies operate using fiat currencies and central banks generally prefer the flexibility this provides. However, gold continues to influence the international monetary system through central bank reserves and investor demand.

Editors note: This post was first published 5 December 2009. Fully updated 17 June 2026 with new charts and numbers and discussion of printing money to buy gold.

Glenn's dedication to educating individuals on wealth protection through precious metals has helped over 2400 clients from New Zealand, Australia, USA and Europe to safeguard their financial futures. Passionate about financial independence and lifestyle freedom, Glenn’s mission is to empower others with the knowledge and tools to thrive in today’s volatile economic environment. When he's not advising on precious metals, Glenn enjoys spending time with his family and pursuing outdoor adventures.

Education: University of Auckland Bachelor of Science

Linkedin: https://www.linkedin.com/in/glenn-thomas-0984a4310/

- Why You Should Become Your Own Central Bank - June 28, 2026

- John Butler, Josh Phair And The Case For Gradual Monetary Change - June 24, 2026

- What Could A Global Currency Reset Mean For New Zealand? - June 19, 2026

It would be interesting to see a table for private gold hold by country.

Scarey, I have more gold than the NZ Government!

Danny,

That would be an insightful piece of information alright. The World Gold Council does track Jewellery, Industrial and Investment demand but we are not aware of them itemizing the investment demand per country – probably because they don’t have the complete information in order to do so. As a large part of private investment in gold is in Over-the-Counter transactions, so it is very difficult to accurately measure.

Although undoubtedly India would be joined by China at the top and New Zealand would be a long way down the list. Also here’s a recent article on how China is about to take over top spot from India as the worlds top Gold consumer…

http://uk.reuters.com/article/idUKLNE5B801V20091209?rpc=401&feedType=RSS&feedName=stocksNews&rpc=401&sp=true

Thanks for your comment.

GSG editors.

I’m not a fan of government’s holding gold. I think if you want to hold gold, then we ought to do it ourselves. As far as currencies are concerned, I’d like to see private crypto-currencies underpinned by gold, if not other currencies. I’d not trust the NZ govt to hold it, as it would probably be plundered. How can we believe that Fort Knox still has its gold reserves. The Fed doesn’t publish the holdings, since its private. It leases it too. I’m not an advocate of such counter-party risks. I personally hold gold shares, because I know with gold in the ground, I don’t have to worry about it being stolen, and it offers an income. Its getting to a point where its almost time to buy.

The Reserve Bank of New Zealand is owned by the Rothschild Family, as are the Reserve banks in most other “western countries”, with the exception of Cuba, Nrth Korea and Iran – hence wars in the Middle East. (Good thing perhaps China bought the U.S.Fed Reserve and gold stocks held by J.P.Morgan) Rothschild took control of Iraq and Libya Reserve Banks – the way paved by blood under the umbrella “fight against terrorism”. Rothschild is now after Iran Reserve Bank by way of Syria. IMF and World Bank is controlled by the Rothschild Group – they have put the peoples of Portugal, Spain, Italy (U.K. although they don’t realize it yet) on their knees and now the peoples of Greece are getting up off their knees to say “NO MORE”. The wars in the Middle East are by Rothschild design to cause total disruption in Europe. How long before NATO troops are ordered in to “regain the peace” or better put take over control.

New Zealand has no gold reserves, Rothschild owns and controls the Reserve Bank and major high street banks. This Elite could put the people of NZ on their knees overnight. Perhaps as soon as 2016.

Hi Helena,

Yes there is a fair bit of evidence backing up what you say.

It is indeed a case of “following the money” in many of these conflicts to see what the rationale is for most of them.

Thanks for taking the time to write an insightful comment.

Gold has to be the most worthless metal ever dreamt about. Asthetic jewelry, a small play in medicine and electronics and conveniently a ‘universal currency’ by horders who monopolise and oversee world curriencies. It is a good thing NZ stays away from gold reserve holdings, as its hit and miss these days whether you have ‘gold’ stock or ‘tungsten’ look-a-like bar… very close atomic weight between these two metals has inspired false gold reserve all over the place … like the load China got as payment from the fed reserve … they was not happy folks … wheres the real stuff going? Well … back to its owners of course – the guys who control the money systems certainly will want to control the ‘universal’ currency as well otherwise owning reserve banks and convential curriencies will mean jack shit … Ive got no gold, but Ive got 112 dollars in the bank … and thats just how I like it.

So we’re broke.

What are the reserves actually used for? The Reserve Banks that hold / buy gold is doing so for what reason? I understand that the US weaponising the dollar causes concern that ones overseas assets my be frozen but for many countries this is unlikely (yes – I know – anything is possible with Trump!) so is the idea that when the dollar finally goes for hyperinflation that gold will support the given countries currency? I’m interesting in the mechanics of what might actually happen. Anyone know?

Great question.

At the most basic level, a country’s reserves are there to provide confidence and flexibility during periods of financial stress.

They can be used for a number of purposes, including:

• Supporting the currency during periods of extreme volatility.

• Providing foreign exchange liquidity if overseas funding markets become stressed.

• Paying for essential imports if access to international capital markets is disrupted.

• Meeting international obligations and foreign currency debts.

• Maintaining confidence among investors, trading partners and credit rating agencies.

• Providing a financial buffer during economic, geopolitical or financial crises.

This is where the debate over gold begins.

The Reserve Bank of New Zealand’s view is that foreign currencies and government bonds are the most useful reserve assets because they can be deployed immediately when needed.

Many other central banks likely agree with that, BUT still choose to hold some gold alongside those assets.

Why?

One reason is that gold is fundamentally different from most other reserve assets.

A US Treasury bond is an asset, but it is also someone else’s liability. The same is true of bank deposits and most foreign currency reserves.

Gold is not.

Gold carries no counterparty risk because it does not depend on another government, bank or institution remaining solvent or honouring its obligations.

That doesn’t mean central banks are necessarily preparing for hyperinflation or a collapse of the US dollar.

However, many appear to be asking the same question individual investors ask:

“If all of my savings are held in currencies and government debt, what happens if those currencies lose purchasing power over time?”

In that sense, some central banks may view gold in a similar way to how many private investors do. Not as a replacement for cash or bonds, but as a form of diversification away from assets that can be created in unlimited quantities.

The freezing of Russia’s foreign exchange reserves in 2022 highlighted another consideration. Some countries became more aware that foreign currency reserves held within the international financial system may not always be as politically neutral as previously assumed.

Whether that justifies holding gold is a matter of debate.

But I think the key point is that central banks don’t generally hold gold instead of foreign currency reserves. They hold it alongside them.

The more interesting question is therefore not “Why do central banks hold gold?”

It’s “Why do some central banks think it is worth holding both, while others, like New Zealand, choose to hold only foreign currency assets?”

Good explanation, Glenn.

I think its ironic that governments talk about “investment” for which they “print” money and create inflation, when in fact what they are doing should be categorised as “expenditure” as there will NOT be a return on the investment.

Here we have an opportunity to INVEST in gold to help protect us from global risk and receive a much greater increase in capital to outweigh any increase in inflation, and recover some of the assinine debt levels notably of the previous, inept gvmt, and expenditure levels exasperatingly continued by the current coalition.