Most people buy gold for the wrong reason.

They focus on whether the gold price will rise, whether now is a good time to buy, or whether gold will outperform other investments. While those questions are understandable, they miss the primary reason people have owned gold for thousands of years.

Gold is not just an investment.

For many investors, savers and even central banks, gold’s most important role is as a form of financial insurance.

Just as people insure their homes, vehicles and businesses against unexpected events, physical gold can help protect purchasing power and financial security against risks that are difficult to predict. These risks include inflation, currency debasement, banking crises, excessive government debt and broader financial instability.

At Gold Survival Guide, we often find that people initially approach gold as an investment opportunity. However, as they learn more about monetary history, banking systems and wealth preservation, many begin to see gold differently. They start viewing physical bullion as a form of financial insurance that can help diversify risk and preserve wealth over the long term.

Importantly, financial insurance is not purchased because you hope disaster will occur. You buy insurance because some risks are too important to ignore.

The same principle applies to gold bullion.

In this guide, we’ll explore why physical gold has served as financial insurance for generations, the risks it may help protect against, and how it can form part of a broader wealth preservation strategy.

Key Takeaways

• Gold is best viewed as financial insurance rather than a speculative investment.

• Physical gold carries no counterparty risk and is not a liability of a bank, company or government.

• Gold has historically helped preserve purchasing power during periods of inflation, currency debasement and financial instability.

• Unlike traditional insurance policies, gold can potentially increase in value while providing protection.

• Many investors use physical gold as part of a broader wealth preservation strategy designed to improve financial resilience during uncertain times.

Table of Contents

- Key Takeaways

- Why Most People Think About Gold Backwards

- What Is Financial Insurance?

- Why Hold Physical Gold As Financial Insurance?

- Wealth Insurance With Upside

- What Risks Can Gold Help Protect Against?

- How Much Financial Insurance Do You Need?

- What Gold Does Not Protect Against

- Physical Gold vs Paper Gold: Which Is Real Financial Insurance?

- Frequently Asked Questions About Gold As Financial Insurance

Estimated reading time: 20 minutes

Why Most People Think About Gold Backwards

When people first consider buying gold, they often focus on one question:

“Will the price go up?”

While price matters, it is arguably the least important reason to own gold.

Most forms of insurance are purchased in the hope they will never be needed. Nobody buys house insurance hoping their home burns down. Nobody buys income protection insurance hoping they cannot work.

Insurance exists to reduce the impact of risks that are difficult to predict but potentially costly if they occur.

Many people spend a great deal of time trying to determine the perfect time to buy gold. While entry price can matter, the more important question is why you own gold in the first place and what role it is intended to play within your portfolio.

If you’re currently wondering whether now is a good time to buy gold, we’ve explored that question in more detail in our guide: “Should I Buy Gold Now or Wait?“.

Gold can be viewed in a similar way.

Rather than asking, “How much money can I make from gold?” a better question may be:

“What risks does gold help protect me from?”

This shift in thinking changes the role gold plays within a portfolio. Instead of being viewed purely as a speculative investment, gold becomes a form of financial insurance designed to help preserve purchasing power and provide diversification during periods of economic uncertainty.

One of the unique characteristics of physical gold is that it combines the protective qualities of insurance with the potential for long-term capital appreciation. This is why many investors view gold as wealth insurance with upside.

Understanding this distinction is the key to understanding why individuals, institutions and central banks continue to hold gold today.

What Is Financial Insurance?

| Traditional Insurance | Financial Insurance |

|---|---|

| House Insurance | Physical Gold |

| Car Insurance | Physical Gold |

| Income Protection Insurance | Physical Gold |

| Protects Physical Assets | Protects Purchasing Power |

| Requires Ongoing Premiums | One-Time Purchase |

| Policy Can Expire | No Expiry Date |

| Pays Out After A Claim | Already In Your Possession |

Most people are familiar with traditional forms of insurance.

We insure our homes against fire, our vehicles against accidents and our income against unexpected events that could affect our ability to earn a living.

Financial insurance works in a similar way.

Rather than protecting physical assets, financial insurance is designed to help protect purchasing power, savings and long-term wealth from risks that may be difficult to predict but could have significant financial consequences.

These risks can include:

- Inflation

- Currency debasement

- Banking crises

- Sovereign debt problems

- Financial market instability

- Loss of confidence in monetary systems

While no investment can eliminate these risks entirely, certain assets have historically helped people preserve wealth during periods of economic uncertainty.

Gold is unique because it has served this role for thousands of years.

Unlike currencies, governments and financial institutions, gold is not dependent on any single issuer or promise. It is a tangible asset that has maintained purchasing power across many different monetary systems and economic cycles.

This is why many investors, institutions and central banks continue to hold gold today—not necessarily because they expect a crisis, but because they recognise the importance of financial insurance within a broader wealth preservation strategy.

Why Hold Physical Gold As Financial Insurance?

You have your house insured to cover against the likes of fire, earthquake, water damage and theft.

So why have financial insurance in the form of gold?

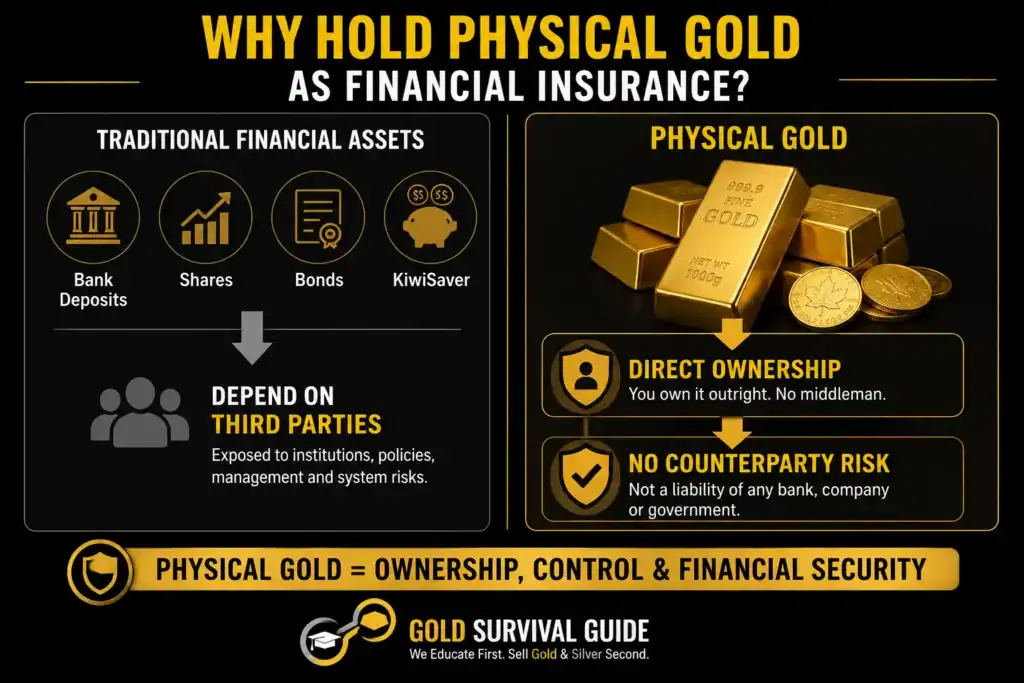

1. Diversify Wealth Outside The Banking System

Most New Zealanders hold a significant portion of their wealth within the traditional financial system through bank deposits, KiwiSaver accounts, managed funds and property.

These assets all play an important role in a financial plan, but they are also connected to the broader financial system.

Physical gold offers something different. It is a tangible asset that can be owned directly and held outside the banking system. For this reason, many investors view gold as a form of financial diversification that complements their other assets rather than replacing them.

The goal is not to avoid the financial system entirely. The goal is to ensure that all of your wealth is not dependent on a single system or institution.

2. Physical Gold Is Not A Bank Liability

One of the unique characteristics of physical gold is that it is not a liability of a bank, government or financial institution.

When money is held in a bank account, it becomes part of the banking system. While banking systems are generally stable, history has shown that financial crises can lead governments and regulators to introduce extraordinary measures.

Examples include bank freezes, withdrawal restrictions and, in some countries, bail-in mechanisms.

Physical gold held directly remains outside those arrangements because it is not dependent on the financial strength of a bank or another institution.

Read more: Bank Failure – Could it Happen in NZ? What does the SVB Bank Failure Mean for NZ?

3. Physical Gold Has No Counterparty Risk

Gold (and silver) is the only financial asset with no counter-party risk. Or put another way, gold is the only financial asset that is not at the same time someone else’s liability.

Compare this to other financial products:

- Bank account – you rely upon the bank remaining solvent. Your savings are the banks liability.

- Shares or stocks – you reply upon the company to continue trading and pay you a dividend or remain of value so your can eventually sell to someone else.

- Bonds – you rely upon the company or government to remain solvent and pay you the coupon amount at maturity or each year.

- Property – usually has a mortgage holder against it. You are also relying upon the leasee or renter to pay the agreed amount of rent each month.

- Exchange traded funds, options, futures, CFD’s – all these financial products involve another counter-party. Such as the broker, or dealer who you rely upon to remain solvent and pay their side of the investment upon due date.

- Kiwisaver Funds – your Kiwisaver is not government guaranteed. See this for more on the risk to Kiwisaver in the case of a bank failure: Kiwisaver and Bank Bail Ins: If a Bank Fails, Are Kiwisaver Funds Affected by the OBR?

On top of this, many of these financial products may be further complicated by the method in which you own them. For example many shares are held in custodian by a broker or bank. So if that financial institution were to fail you may find your shares are actually held as liabilities on their books.

Read more: Gold Mining Shares vs Physical Gold Bullion – Which to Buy? >>

4. Gold Has Retained Value For Thousands Of Years

Throughout history, currencies have come and gone. Governments have risen and fallen. Companies have succeeded and failed.

Gold has persisted through all of these changes.

While the price of gold can fluctuate over shorter periods, it has maintained purchasing power across centuries and multiple monetary systems. This is one reason many investors believe gold is more valuable than paper currencies that can be created without limit.

And why gold is viewed not as a speculation, but as a long-term store of value designed to help preserve wealth across generations.

Unlike all the above mentioned financial assets gold has never in all of history “gone to zero” and been worth nothing. Odds are that despite technological changes gold will be worth something in the future. And will likely hold its purchasing power just as it has done for thousands of years.

The often quoted but still valid example is an ounce of gold in roman times bought a fine toga and sandals. Today an ounce of gold still buys a fine mens suit and shoes.

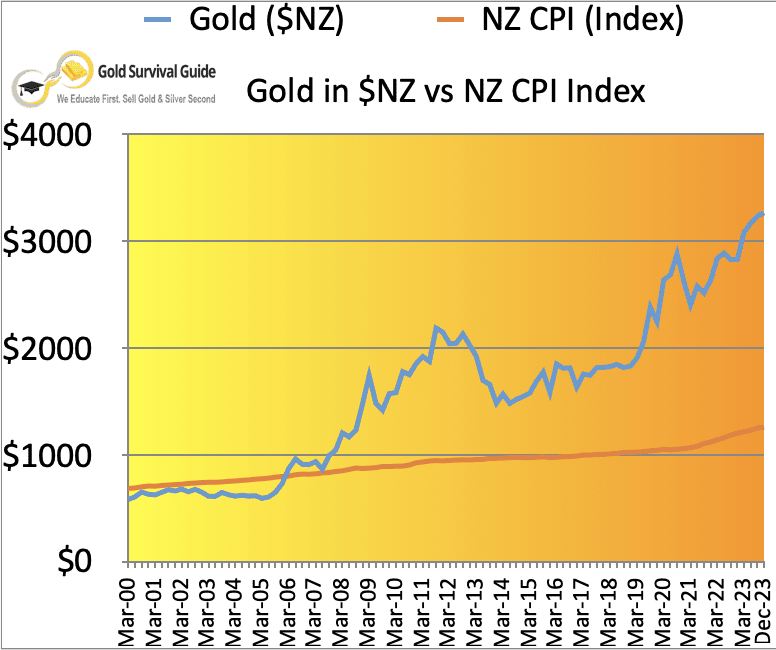

While historical examples help illustrate the concept, we can also look at more recent New Zealand data. Since 2000, the New Zealand Consumer Price Index (CPI) has risen approximately 83%, while the NZ dollar gold price has risen approximately 460%. (That doesn’t include the hefty rise in gold for the last few years either).

Although past performance never guarantees future results, this provides a real-world example of gold preserving — and in this case increasing — purchasing power over a long period of time.

For a detailed analysis of the data behind this chart, see our article: The NZD Gold Price vs Inflation: Analysing the Performance and Break-Even Potential.

5. Maintain Greater Control Over Your Wealth

One of the advantages of physical bullion is direct ownership.

Unlike many financial assets, physical gold can be held privately, stored securely and accessed without relying on a financial institution.

This gives investors a greater degree of control over a portion of their wealth.

While governments throughout history have occasionally imposed capital controls, restrictions or asset confiscation measures during periods of crisis, the broader lesson is that diversification and direct ownership can provide additional flexibility during uncertain times.

While this may seem extreme in New Zealand, there are countless historical occurrences where gold has provided wealth protection from asset confiscation. Where an authoritarian government has confiscated property and it is the gold insurance “policy” that has allowed families to escape.

Wealth Insurance With Upside

Traditional insurance policies are designed to protect you against specific risks.

House insurance protects your home.

Car insurance protects your vehicle.

Income protection insurance protects your ability to earn an income.

In each case, you pay a cost for protection and hope you never need to make a claim.

Gold is different.

While many investors view physical gold as a form of financial insurance, it also has the potential to preserve purchasing power and appreciate in value over time.

This combination makes gold unique.

It can help protect wealth during periods of economic uncertainty while also providing the possibility of long-term capital appreciation.

This is why we often describe gold as “wealth insurance with upside”.

You do not buy gold hoping for a financial crisis, just as you do not buy house insurance hoping your home burns down.

However, unlike most insurance products, gold has historically provided both protection and the potential for long-term growth.

This combination of resilience and upside is one of the reasons gold continues to play an important role in portfolios around the world.

Historically, an investment in physical gold made 20 years ago would be worth substantially more today while still providing the benefits of financial insurance throughout that period.

So just like planting a tree, the best time to buy gold for financial insurance was 20 years ago, but the next best time is today.

Precious metals likely have a lot higher to run to reach their potential maximum historical valuations. Read more: How Do You Value Gold | What Price Could it Reach?

For a video presentation on this topic see: Presentation – Gold & Silver: Wealth Insurance with Upside

What Risks Can Gold Help Protect Against?

When you take out an insurance policy you need to give some thought as to what you are covered for. Sometimes you pay a higher premium to get greater coverage for less likely but potentially very costly risks.

Gold can play many different roles within a portfolio, but one of its most important functions is helping to manage risk.

While many people associate gold with financial crises and systemic events, its potential benefits extend beyond extreme scenarios. Gold has historically helped investors protect purchasing power, diversify portfolio risk and build financial resilience during periods of economic and political uncertainty.

Let’s look at some of the key risks that gold may help protect against.

1. Inflation and Loss of Purchasing Power

One of the greatest long-term threats to wealth is not usually a market crash or financial crisis. It is the gradual erosion of purchasing power caused by inflation.

Inflation occurs when the cost of goods and services rises over time, reducing what each dollar can buy. While inflation may seem relatively small in any given year, its cumulative effect over decades can significantly reduce the real value of savings held in cash.

Gold has historically helped preserve purchasing power over long periods of time.

While the quoted price of gold can fluctuate in the short term, its ability to retain value over centuries is one of the reasons it has been used as money and a store of wealth throughout history. The often-quoted example is that an ounce of gold in Roman times could buy a fine toga and sandals. Today, an ounce of gold can still purchase a quality men’s suit and shoes.

For this reason, many investors view gold as a hedge against the long-term effects of inflation and currency debasement.

2. Gold Can Help Diversify Portfolio Risk

One of the challenges many investors face is that a large portion of their wealth is often concentrated in similar types of assets.

Property, shares, managed funds, KiwiSaver investments and bank deposits can all be influenced by the health of the broader economy and financial system.

Gold is different.

While gold does not always move in the opposite direction to other assets, it has often behaved differently from shares during periods of economic uncertainty. Our analysis of the Dow Gold Ratio over the past century highlights how gold and shares can perform very differently across long-term market cycles.

This means gold can provide diversification within a portfolio.

In simple terms, diversification means not having all your eggs in one basket.

If all of your wealth is tied to assets that are affected by the same economic conditions, your overall financial risk may be higher than you realise.

By owning a portion of your wealth in physical gold, investors can add an asset that is not directly dependent on corporate profits, property markets, bank performance or government policies.

For this reason, many investors view gold as a useful complement to traditional investments and an important component of a broader financial insurance strategy.

3. Financial Resilience During Uncertain Times

Periods of economic, political and financial uncertainty can create challenges for investors.

Financial crises, geopolitical tensions, banking instability, sovereign debt concerns and sudden shifts in market sentiment can all affect traditional assets and increase uncertainty about the future.

While no asset can eliminate these risks entirely, gold has historically been viewed as a safe-haven asset during times of heightened uncertainty.

One reason for this is that gold is globally recognised, highly liquid and not dependent on the financial strength of a particular company, government or institution.

Throughout history, investors have often turned to gold during periods of market stress and loss of confidence in financial systems. While gold prices can still fluctuate, many investors value the stability and reassurance that comes from owning a tangible asset that has maintained its role as a store of wealth for thousands of years.

For this reason, physical gold is often included within a broader wealth preservation strategy designed to improve financial resilience during uncertain times.

How Much Financial Insurance Do You Need?

One of the most common questions investors ask is:

“How much gold should I own?”

There is no universal answer because every person’s financial situation, objectives and risk tolerance are different.

However, many investors view precious metals in the same way they view other forms of insurance. The goal is not necessarily to maximise returns. The goal is to ensure that a portion of their wealth is protected against risks that may affect traditional financial assets.

Common allocation ranges often discussed include:

5%

Suitable for investors seeking modest diversification and exposure to precious metals.

10%

Often considered a balanced allocation for those wanting a meaningful level of financial insurance while maintaining broad exposure to other asset classes.

15–20%

Typically chosen by investors who have stronger concerns about inflation, currency debasement, financial system risk or long-term wealth preservation.

The appropriate allocation will depend on your individual circumstances and objectives.

If you’d like a more detailed discussion, see our guide:

What Percentage of Gold and Silver Should Be In My Portfolio?

That article explores the factors that may influence how much precious metals exposure is appropriate for different investors.

What Gold Does Not Protect Against

When purchasing house or car insurance, it pays to read the fine print.

Insurance policies often contain exclusions, limitations and conditions that determine when cover applies and when it doesn’t.

Physical gold is different.

There is no insurance company deciding whether your claim is approved. Gold does not expire, it cannot be cancelled and it does not rely on a promise from a third party.

However, there is still an important piece of fine print that many investors overlook.

Not all forms of gold provide the same level of financial insurance.

Many people assume that gold ETFs, futures contracts, mining shares and other paper gold investments offer the same protection as owning physical bullion. While these investments may track the gold price to varying degrees, they do not provide the same benefits as directly owning physical gold.

If the goal is financial insurance, the type of gold you own matters just as much as the decision to own gold itself.

This brings us to one of the most important distinctions investors need to understand: physical gold versus paper gold.

Physical Gold vs Paper Gold: Which Is Real Financial Insurance?

For gold to work as financial insurance, the type of ownership matters. Physical bullion held directly is very different from paper gold products whose value depends on another party remaining solvent.

You need to buy physical gold held in your own possession, in order for there to be no counterparty risk.

So if you want gold as wealth insurance you should avoid any of the following that have counterparty risk:

- Gold mining shares

- Exchange Traded Fund’s (ETF’s)

- Gold futures

- Gold options

- Contracts for Difference (CFD’s)

Are we saying don’t buy any of the above? No, just don’t confuse them with physical gold as financial insurance. A share in a gold mining company is a speculative investment. Not financial insurance.

In a worst case scenario, like a financial crisis even worse than the last, gold derivatives could well be totally worthless. Trading rules could be altered stopping you gaining maximum profits. Or the counterparty could default leaving you with nothing at all.

Read more: Paper Gold vs Physical Gold – What Should You Buy? >>

The Risk With Gold Futures, Even if the Gold Price Rises

If gold rises massively, margin requirements could rise massively too. When trading futures you are required to put a certain amount of cash up and then this is leveraged.

However there are historical examples in other commodities where there has been a large jump in price. The futures exchange hiked margins massively, meaning traders had to deposit large amounts of capital in order maintain their position. Even though the price had risen!

Why Financial Insurance Matters More Than Ever In New Zealand

Every country faces its own unique economic challenges and risks. While New Zealand remains one of the most stable and well-governed countries in the world, many New Zealanders have a significant proportion of their wealth concentrated in a relatively small number of areas.

For example, many households rely heavily on:

- Property

- Bank deposits

- KiwiSaver

- Shares and managed funds

While these assets can play an important role in a financial plan, they are all connected, to varying degrees, to the broader financial system.

Physical gold offers something different.

It is a tangible asset that sits outside the banking system and does not depend on the performance of any company, fund manager or government institution.

At Gold Survival Guide, we often find that people initially approach precious metals as an investment. Over time, many come to view physical bullion as a form of diversification and financial insurance that complements the rest of their portfolio rather than replacing it.

The goal is not to predict economic disasters or financial crises.

The goal is to recognise that uncertainty is a normal part of life and to build resilience into a long-term wealth preservation strategy.

Frequently Asked Questions About Gold As Financial Insurance

Many investors view physical gold as a form of financial insurance because it has historically helped preserve purchasing power during periods of inflation, currency debasement, financial crises and economic uncertainty. Unlike traditional financial assets, physical gold is not dependent on the performance of a company, bank or government institution.

Gold has historically helped preserve purchasing power over long periods of time. While its price can fluctuate in the short term, many investors hold gold as a hedge against the erosion of purchasing power caused by inflation.

Unlike shares in a company, gold is a tangible asset with intrinsic value and a long history of use as money and a store of wealth. While its market price can rise and fall, gold has maintained value across many different monetary systems for thousands of years.

Physical gold and gold ETFs serve different purposes. Physical gold provides direct ownership of bullion, while ETFs provide exposure to the gold price through a financial product. Investors seeking financial insurance often prefer physical ownership because it removes many forms of counterparty risk.

Central banks around the world continue to hold gold as part of their reserves because it is a globally recognised monetary asset that is not tied to the liabilities of another institution. Gold can provide diversification and resilience within a reserve portfolio.

The appropriate allocation depends on your financial goals, risk tolerance and existing assets. Many investors allocate between 5% and 20% of their portfolio to precious metals, although individual circumstances vary.

Gold can be both. However, many long-term owners view gold primarily as financial insurance and wealth protection, with potential investment gains being a secondary benefit.

Gold and silver each have different characteristics. Gold is generally viewed as the more established wealth preservation asset, while silver often offers greater volatility and potential upside. Many investors choose to own a combination of both.

Conclusion

Most people spend their lives insuring the things they own.

They insure their homes, vehicles, businesses and health because they understand that unexpected events can happen.

Yet many people hold the majority of their wealth in assets that are exposed to inflation, currency debasement, banking system risk and broader financial uncertainty without considering how they might protect themselves from those risks.

Physical gold offers a different approach.

For thousands of years, it has served as a store of value, a monetary asset and a form of financial insurance. It is one of the few assets that is not simultaneously somebody else’s liability and has continued to retain purchasing power across generations.

This does not mean gold is a guarantee against every risk, nor does it mean investors should abandon other asset classes. Rather, gold can play an important role within a diversified wealth preservation strategy.

At Gold Survival Guide we believe that gold is wealth insurance first and an investment second. Ownership matters more than prediction, and long-term wealth preservation matters more than short-term speculation.

The best time to think about financial insurance is before you need it.

If you’re considering adding precious metals to your portfolio, take the time to understand the role they can play within your broader financial strategy and determine what level of financial insurance is appropriate for your circumstances.

Head on over to our online store and see what gold and silver financial insurance products are available today: Buy gold and silver.

Editors Note: This article was first published 4 July 2018. Fully updated 2 June 2026.

Glenn's dedication to educating individuals on wealth protection through precious metals has helped over 2400 clients from New Zealand, Australia, USA and Europe to safeguard their financial futures. Passionate about financial independence and lifestyle freedom, Glenn’s mission is to empower others with the knowledge and tools to thrive in today’s volatile economic environment. When he's not advising on precious metals, Glenn enjoys spending time with his family and pursuing outdoor adventures.

Education: University of Auckland Bachelor of Science

Linkedin: https://www.linkedin.com/in/glenn-thomas-0984a4310/

- How Much Gold Does New Zealand Have? Why The Reserve Bank Holds Zero Gold Reserves - June 17, 2026

- Gold’s 2026 Correction: What Happens Next? - June 17, 2026

- Gold Overtakes Treasuries While Silver Sentiment Hits Extreme Fear - June 10, 2026