Table of Contents

- What Is A Global Currency Reset?

- Why Are People Talking About It Again?

- Why Does Gold Keep Appearing In These Discussions?

- Does New Zealand Have A Seat At The Table?

- Does New Zealand’s Lack Of Gold Reserves Matter?

- What About New Zealand’s Gold In The Ground?

- What Could A Currency Reset Mean For New Zealand?

- What Should Investors Take From This?

- Frequently Asked Questions About Global Currency Resets

- Continue Learning:

Talk of a “global currency reset” has been circulating for years.

Some believe the US dollar is losing its dominance. Others point to the rise of BRICS nations, record central bank gold purchases and growing efforts to reduce reliance on the dollar in international trade. More recently, the freezing of Russia’s foreign exchange reserves and rising geopolitical tensions have renewed questions about how the international monetary system might evolve in the years ahead.

The problem is that the term global currency reset can mean very different things to different people.

For some, it refers to the emergence of a new reserve currency. For others, it means a greater role for gold, a gold-backed BRICS currency, expanded use of IMF Special Drawing Rights (SDRs), or a more multipolar monetary system where several major currencies share influence.

Monetary systems do change. The world has moved from the classical gold standard to Bretton Woods, and from Bretton Woods to the modern fiat currency system we live under today.

If the international monetary system were to change again, where would New Zealand fit?

Would New Zealand have any influence over the process? Does the country’s lack of official gold reserves matter? And what impact could a changing monetary system have on New Zealand investors, savers and businesses?

In this article we’ll examine what people mean by a global currency reset, why the discussion has intensified in recent years, and what it might mean for New Zealand.

What Is A Global Currency Reset?

One of the challenges when discussing a “global currency reset” is that there is no universally accepted definition of the term.

Different people use it to describe very different scenarios.

Some use it to refer to the emergence of a new global reserve currency. Others mean a larger role for gold within the international monetary system. Some are referring to the growth of BRICS and efforts to reduce reliance on the US dollar, while others believe institutions such as the International Monetary Fund (IMF) could play a larger role through Special Drawing Rights (SDRs).

Monetary systems rarely change through a single dramatic event.

The world moved from the classical gold standard to the Bretton Woods system after World War II. Bretton Woods eventually gave way to today’s fiat currency system after the United States suspended dollar convertibility into gold in 1971.

Rather than a single event, a global currency reset is better thought of as a potential evolution of the international monetary system.

The question is not whether the world will wake up one morning to a completely new currency system. It is whether the trends we are seeing today could gradually lead to a different monetary order over time.

By the early 2030s, we may look back and realise that reserve diversification, geopolitical realignment and changes to international trade settlement reshaped the system gradually, rather than through a single dramatic reset.

Why Are People Talking About It Again?

Discussion of a global currency reset is not new.

What has changed is the number of developments pointing in the same direction.

One of the biggest has been the freezing of Russia’s foreign exchange reserves following its invasion of Ukraine in 2022. For many countries, this highlighted a risk that had previously received little attention. Reserve assets held within the international financial system may not always be politically neutral.

At the same time, central banks have been buying gold at the fastest pace seen in decades. After being net sellers of gold during much of the 1990s and early 2000s, central banks became net buyers following the Global Financial Crisis. Since 2022, purchases have exceeded 1,000 tonnes per year on average.

Growing geopolitical tensions have also encouraged some countries to diversify their reserves and trade relationships. Discussions around BRICS expansion, alternative payment systems and settlement mechanisms outside the US dollar have all gained momentum in recent years.

Rising government debt levels are another factor. Many developed nations now carry debt burdens that would have been difficult to imagine a generation ago. While high debt does not automatically lead to a monetary reset, it raises questions about how those debts will ultimately be managed.

Supply chains are also becoming less global and more regional. The trend towards reshoring, friend-shoring and strategic competition between major powers points towards a more fragmented world economy than the one that emerged after the Cold War.

None of these developments prove that a global currency reset is imminent. Together, however, they help explain why discussions about reserve currencies, gold and the future of the international monetary system have become more common.

Why Does Gold Keep Appearing In These Discussions?

One reason gold appears so frequently in discussions about the future of the monetary system is that it has played a role in almost every major monetary system of the past two centuries.

Monetary Systems Change More Often Than Many People Realise

Classical Gold Standard → pre-1914

Gold Exchange Standard → 1920s-1930s

Bretton Woods System → 1944-1971

Modern Fiat Currency System → 1971-Present

The current monetary system is less than 55 years old. It is not the first international monetary system, and it is unlikely to be the last.

Under the classical gold standard, currencies were directly linked to gold. Under the Bretton Woods system established after World War II, the US dollar was convertible into gold and served as the foundation of the international monetary system. Even after that link was broken in 1971, central banks continued to hold thousands of tonnes of gold in their reserves.

Today, gold no longer formally backs any major currency.

However, it remains one of the world’s most widely held reserve assets. In fact, the European Central Bank recently reported that gold now ranks ahead of both US Treasuries and the euro as a global reserve asset.

Unlike government bonds, bank deposits or foreign currencies, gold carries no counterparty risk. It is not dependent on another government, central bank or financial institution honouring its obligations. For this reason, many countries continue to view gold as a useful reserve asset despite no longer operating under a gold-backed monetary system.

If gold had become irrelevant to the international monetary system, there would be little reason for central banks to hold it at all. Yet central banks have been adding to their gold reserves at the fastest pace seen in decades.

[We recently examined that trend and New Zealand’s unusual position of holding no official gold reserves.]

That does not mean gold will necessarily play a formal role in any future monetary system.

Many possibilities have been proposed over the years, ranging from a return to some form of gold backing, to a larger role for Special Drawing Rights (SDRs), to a more fragmented system in which several reserve assets coexist.

Gold continues to be treated differently from most other assets. That helps explain why discussions about reserve currencies and monetary reform so often lead back to gold.

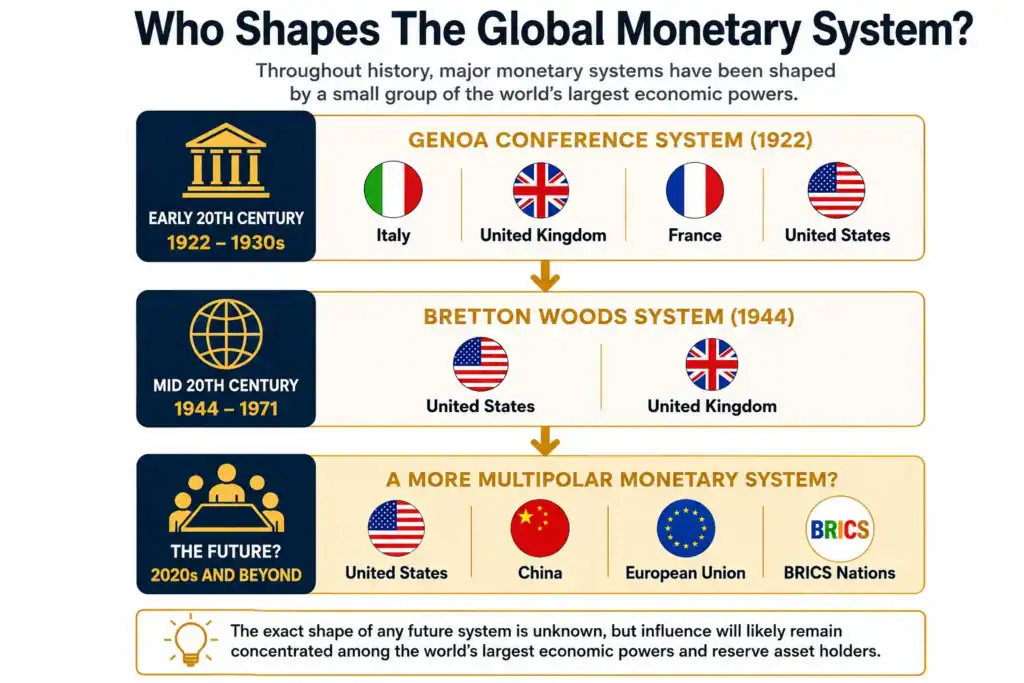

Does New Zealand Have A Seat At The Table?

If the international monetary system were to undergo significant change, the countries shaping those decisions would almost certainly be the world’s largest economies and reserve currency issuers.

Historically, countries that helped shape major monetary arrangements were often among the world’s largest economic powers and holders of major reserve assets, including gold.

From Genoa in 1922 to Bretton Woods in 1944, the nations helping design the monetary system were generally major powers rather than small economies on the periphery.

The Bretton Woods system was designed primarily by the United States and United Kingdom following World War II. Today, discussions around reserve currencies, international trade settlement and financial architecture are dominated by countries such as the United States, China, members of the European Union and increasingly the BRICS nations.

New Zealand occupies a very different position.

New Zealand’s Position In The Global Monetary System

• Less than 0.3% of global GDP

• NZD is not a global reserve currency

• No official gold reserves

• Highly trade-dependent economy

• Relies on foreign currency reserves rather than gold

New Zealand represents less than 0.3% of global GDP and the New Zealand dollar accounts for only a small share of global foreign exchange reserves and international trade settlement.

Unlike the United States, New Zealand does not issue a reserve currency. Unlike China, it does not possess the economic scale to influence global monetary policy. And unlike many countries, New Zealand holds no official gold reserves.

That does not mean New Zealand would be unaffected by changes to the international monetary system.

As a small, trade-dependent nation, New Zealand is heavily influenced by developments in global financial markets, international trade and reserve currency arrangements.

New Zealand would be more likely to have to adapt to a changing monetary system than help design it.

The key question is not how New Zealand can shape the next monetary system, but how well positioned it would be if the system changes around it.

Does New Zealand’s Lack Of Gold Reserves Matter?

Whether New Zealand’s lack of gold reserves matters depends largely on how one views the purpose of a country’s reserve assets.

Supporters of the current approach would argue that the Reserve Bank’s primary responsibility is to maintain highly liquid reserves that can be deployed quickly during periods of financial stress. From that perspective, foreign currencies, government bonds and other liquid assets may be more useful than gold.

This is the view the Reserve Bank of New Zealand has taken for many years. The Bank has repeatedly stated that gold does not meet its liquidity requirements and has shown little interest in rebuilding official gold reserves.

Others argue that many central banks continue to hold gold despite having access to the same foreign currency reserves and government bond markets as New Zealand.

Countries With Similar GDP To New Zealand And Their Gold Reserves

Countries with economies broadly comparable in size to New Zealand continue to hold official gold reserves. New Zealand remains one of the few developed nations with no official gold holdings at all.

| GDP (US$ Billions, 2026 IMF) | Gold Reserves (Tonnes) | |

| Peru | 380.9 | 34.7 |

| Portugal | 380.6 | 383 |

| Kazakhstan | 360.5 | 354 |

| Algeria | 317.2 | 174 |

| Greece | 307.6 | 115 |

| New Zealand | 278.6 | 0 |

| Hungary | 271.1 | 110 |

| Iraq | 264.8 | 171 |

| Qatar | 217.4 | 115 |

Supporters of holding gold argue that reserve assets should do more than provide day-to-day liquidity. They should also help diversify a country’s exposure to financial, monetary and geopolitical risks.

Unlike government bonds or foreign currency reserves, gold carries no counterparty risk. It is not dependent on another government, central bank or financial institution honouring its obligations.

This could become particularly relevant if the international monetary system evolves in ways that place greater importance on gold or other reserve assets.

New Zealand’s position is unusual.

Many countries choose to hold both foreign currency reserves and gold. New Zealand is one of a relatively small number of developed countries that holds no official gold reserves.

What About New Zealand’s Gold In The Ground?

Whenever New Zealand’s gold reserves are discussed, another question often arises.

If New Zealand produces gold and still has significant gold resources in the ground, does it really matter that the Reserve Bank holds none?

The answer depends on which type of gold we are talking about.

Many people assume that gold held by a central bank, gold owned by private citizens and gold still sitting in the ground are essentially the same thing. They are not.

Not All Gold Is The Same

| Type | Who Owns It? | Can It Be Used As Official Reserves? |

|---|---|---|

| Official Gold Reserves | Central Banks | Yes |

| Private Gold | Individuals & Businesses | No |

| Gold In The Ground | Nobody Yet (or Companies) | No |

These three categories are often confused, but they serve very different roles within the economy and the monetary system.

Gold resources in the ground, for example, must first be discovered, permitted, mined, refined and sold before they become usable assets.

New Zealand remains a gold-producing nation and significant gold resources still exist within the country. However, those resources are very different from official gold reserves held by a central bank.

We have previously explored whether New Zealand could build official gold reserves using royalties from domestic gold production. That debate highlights the distinction between gold being mined within a country and gold actually held as part of a nation’s official reserves.

If the international monetary system were to change, it is official reserves rather than underground resources that would be most relevant to discussions about reserve currencies and monetary policy.

For this reason, New Zealand’s gold resources and New Zealand’s official gold reserves are best thought of as two separate questions.

What Could A Currency Reset Mean For New Zealand?

The phrase “global currency reset” often creates images of an overnight financial collapse or the sudden replacement of existing currencies.

Major monetary changes are usually far more gradual.

The Bretton Woods system did not disappear overnight. Nor did the transition away from the gold standard. These changes unfolded over years and, in some cases, decades.

If another significant shift occurs in the international monetary system, the impact on New Zealand would depend largely on the nature of that change.

Scenario 1: No Formal Reset

One outcome is that the international monetary system continues evolving gradually rather than experiencing a formal reset.

The US dollar remains the dominant reserve currency, but countries continue to diversify their reserves and trading relationships, while alternative payment systems and regional trade arrangements become more common.

Under this scenario, most New Zealanders may barely notice the transition taking place.

Scenario 2: Gold Becomes More Important

Another possibility is that gold plays a larger role within the international monetary system.

This does not necessarily mean a return to a traditional gold standard. However, gold could become increasingly important as a reserve asset, collateral asset or settlement asset between countries.

If this occurred, countries holding substantial gold reserves may gain additional flexibility and options within the evolving monetary system.

New Zealand would enter such a system without any official gold reserves.

Whether that would prove significant remains uncertain, but it is one reason many observers continue to question New Zealand’s decision to hold none.

Scenario 3: A More Multipolar Monetary System Emerges

A third possibility is the emergence of a more multipolar system.

Rather than one dominant reserve currency, international trade and reserves could become increasingly diversified across multiple currencies and assets.

This might include:

- The US dollar

- The Chinese yuan

- Gold

- Regional payment and settlement systems

- Special Drawing Rights (SDRs)

Many of the developments discussed in recent years, including BRICS initiatives, central bank gold buying and efforts to reduce reliance on the US dollar, point in this direction.

Whether these efforts ultimately succeed remains uncertain.

They do demonstrate that many countries are actively exploring alternatives to a purely dollar-centric system.

The Key Point For New Zealand

New Zealand will not determine how the international monetary system evolves.

Those decisions will largely be shaped by major economies and reserve-holding nations.

What New Zealand can control is how prepared it is to adapt to whatever system eventually emerges.

Worth Watching: 2030–2032

Scottsdale Mint CEO Josh Phair recently suggested that by 2030-2032 we may look back and realise the monetary system changed significantly, even though those changes occurred gradually over many years.

Whether that proves correct remains to be seen. However, it reflects the view that major monetary changes are more likely to be evolutionary than revolutionary.

Related: Why The 2030-2032 Timeline Is Worth Watching

What Should Investors Take From This?

One lesson from monetary history is that financial systems do change.

The gold standard ended. Bretton Woods ended. The current fiat currency system replaced both.

What nobody knows is exactly how the next phase of the international monetary system will develop, or how long any transition might take.

Will the US dollar remain dominant? Will gold play a larger role? Will a more multipolar monetary system emerge?

Major monetary changes are usually recognised more easily in hindsight than in advance.

For investors, the more useful question may not be what the next monetary system will look like, but how to prepare for a range of possible outcomes.

Many central banks continue to hold reserve assets such as gold not because they know exactly what the future holds, but because they recognise that uncertainty exists.

Individual investors can do the same.

The goal is not to predict the future with perfect accuracy. It is to understand the risks, recognise the limits of prediction and build resilience accordingly.

Related: Why You Should Become Your Own Central Bank

Frequently Asked Questions About Global Currency Resets

A global currency reset is a broad term used to describe a significant change in the international monetary system. Different people use it to mean different things, including the emergence of a new reserve currency, a greater role for gold, the expansion of BRICS influence, increased use of SDRs, or a more multipolar monetary system.

Nobody knows for certain. However, several developments have intensified discussion around the topic, including rising government debt, geopolitical tensions, reserve diversification and efforts by some countries to reduce reliance on the US dollar.

At present, the US dollar remains the dominant reserve currency and is deeply embedded in global trade and finance. While BRICS nations are exploring alternative payment systems and settlement mechanisms, replacing the dollar entirely would be a complex process likely to take many years, if it happened at all.

It is possible, but not guaranteed. Gold played a central role in previous monetary systems and remains widely held by central banks today. Even if currencies never return to a formal gold standard, gold could continue to play an important role as a reserve asset, collateral asset or settlement asset between nations.

Central banks have become net buyers of gold since 2010. Common reasons include reserve diversification, concerns about inflation, geopolitical tensions, sanctions risk and reducing dependence on any single foreign currency.

No. The Reserve Bank of New Zealand currently holds zero official gold reserves. Most of New Zealand’s gold reserves were sold during the 1960s, with the final remaining gold sold in 1991.

Related: How Much Gold Does New Zealand Have? Why The Reserve Bank Holds Zero Gold Reserves

Yes. There is nothing preventing New Zealand from purchasing gold if policymakers believed it was appropriate. However, the Reserve Bank has consistently stated that gold does not meet its liquidity requirements and has shown little interest in rebuilding official gold reserves.

Supporters of the current approach argue that foreign currency reserves and government bonds are more useful for day-to-day liquidity needs. Others argue that gold provides diversification and carries no counterparty risk. This debate is one reason New Zealand’s reserve policy continues to attract attention.

The impact would depend on the nature of the change. New Zealand is unlikely to shape the future international monetary system, but it would need to adapt to any significant changes in reserve currencies, trade settlement mechanisms or global financial markets.

Monetary systems change over time. Rather than attempting to predict the exact form of any future system, many investors focus on diversification, resilience and understanding how different assets perform under different economic conditions.

Gold has played a role in most major monetary systems of the past two centuries and remains widely held by central banks today. The European Central Bank recently reported that gold now ranks ahead of both US Treasuries and the euro as a global reserve asset. Its long monetary history and lack of counterparty risk are two reasons it continues to feature prominently in discussions about the future of the international monetary system.

No. Gold resources in the ground, privately owned gold and official central bank gold reserves are three different things. Gold held by a central bank is an official reserve asset. Gold still in the ground must first be discovered, permitted, mined and refined before it becomes a usable asset.

Continue Learning:

Silver’s possible role in a currency collapse: What Use Will Silver Coins be in New Zealand in a Currency Collapse?

The role gold may play in the global monetary system change: If the US Dollar Collapses, What Will Gold be Priced in?

Editors Note: Originally published 10 October 2017. Fully rewritten 19 June 2026 to include latest GDP and official gold reserves.

Glenn's dedication to educating individuals on wealth protection through precious metals has helped over 2400 clients from New Zealand, Australia, USA and Europe to safeguard their financial futures. Passionate about financial independence and lifestyle freedom, Glenn’s mission is to empower others with the knowledge and tools to thrive in today’s volatile economic environment. When he's not advising on precious metals, Glenn enjoys spending time with his family and pursuing outdoor adventures.

Education: University of Auckland Bachelor of Science

Linkedin: https://www.linkedin.com/in/glenn-thomas-0984a4310/

- Why You Should Become Your Own Central Bank - June 28, 2026

- John Butler, Josh Phair And The Case For Gradual Monetary Change - June 24, 2026

- What Could A Global Currency Reset Mean For New Zealand? - June 19, 2026

Every year foreign companies mine and remove from our shores about 10 tons of gold. Seems crazy that the NZ Government does not mine this gold for our benefit. Why on earth is that???

Thanks for your comment John. You could argue there is some benefit to the country in that some taxes will be paid on this activity. On top of the people employed etc. However you are right that unlike some other countries, NZ does not have a “royalty” that a miner must pay to the government. But we could also argue as to how much benefit such a royalty would have. Likewise if the government were to mine this gold themselves how effective would that be? How effective are government at anything they do? We make an argument in this old post that the best benefit of gold is when it is allowed to circulate freely… https://goldsurvivalguide.co.nz/oceania-gold-mine-expansion-why-the-greens-should-be-embracing-gold/

You are wrong. The Reserve Bank dies have some gold. I rang them a couple of years ago and asked. They said they have 1 ounce. I would guess they have a 1 ounce gold coin framed, hanging on a wall somewhere. They said, when asked, that they had no intention of buying any. Since then I have scratched my head and wondered how people with no idea about where the world is headed and works get employed there, that includes the Governor. I have a better idea than them.

Sorry Andy. We stand corrected! That’s one less ounce they need to buy I guess. And that is probably the point, that the cogs in the machine aren’t meant to know what they are doing. As we said best we all act as our own central banks. Because this is unlikely to change in a hurry.