Darryl Schoon gives his thoughts as to how we have seen the end of the beginning of this financial and monetary crisis but how the worst is still to come. However he remains ever optimistic about what will follow. In our discussions with him a few years back he outlined how he has been heavily influenced by inventor and deep thinker Buckminster Fuller. Like Fuller he expects a better world to follow the coming breakdown and collapse. While we hope he is correct, we also plan for the worst. As he recommends, holding physical gold and silver is part of this preparation. (The post also contains a video of him on the same topic but from a slightly different angle if you prefer to watch and listen than read too)…

2014 THE END OF THE BEGINNING

The economic crisis has entered a new stage; and when it ends, the bankers’ world – a paper edifice composed of credit and debt – will be in flames.

In Time of the Vulture: How to Survive the Crisis and Prosper in the Process (2007), I predicted a cataclysmic economic crisis was about to occur. At the time, few believed a severe financial crisis likely. It had been seven years since the 2000 dot.com bubble collapse and signs of recovery were everywhere.

But, in 2006, Bill Bonner in his commentary, Ponzi Economy, explained why a crisis was coming. The US economy, fueled by a two-decade credit boom, had become a “ponzi economy”, a gigantic speculative bubble, about to burst.

PONZI ECONOMY

…Everybody likes a credit boom. They all believe they have more money. This is the dirty little secret of modern central banking. It only works by stealth and fraud – silently debauching the currency so that people make mistakes.

The businessman believes there is more demand for his products than there really is. The consumer believes he has more purchasing power than he really has. The lender believes the borrower is a better risk than he really is. All these mistaken judgments lead to spending, investing and lending – which look to all the world like a bona-fide boom.

But it is an ersatz boom, a public spectacle, founded on fraud, expanded into farce, and ending ultimately in disaster. Eventually, everyone gets too stretched out on credit.

Then, the bubble finally finds a pin somewhere, and the air wheezes out. That’s the part that no one cares for, because it is when people discover that they’ve made mistakes, that they’ve over-reached, and that they’ve been had.

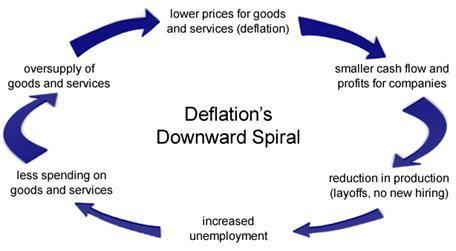

If, as we believe, we’re at the beginning of the disaster stage, the Fed’s real enemy is not inflation at all; it’s deflation. Typically, a credit contraction shrinks everything down with it. Earnings go down. Consumer spending is reduced. GDP growth falls…or even goes negative. And prices for most financial assets dive.

Bill Bonner, www.dailyreckoning.com, July 10, 2006

If, as we believe, we’re at the beginning of the disaster stage, the Fed’s real enemy is not inflation at all; it’s deflation – Bill Bonner. Bonner was right and, now, 6 ½ years later the beginning of the disaster stage is over. The end of the beginning has been reached. The disaster comes next.

THE REAL ENEMY – DEFLATION

… When the dot.com bubble burst in 2000, it was deflation that Greenspan feared. Now, interrupted by an intervening property and investment bubble, irrespective of what the pundits say, it is not inflation, but deflation that keeps Central Bankers worrying and awake at night. The nightmare is not yet over. It has not yet even begun.

Schoon, Time of the Vulture, 2007

Deflation was the cause of the Great Depression and the possibility of another massive deflationary collapse—a black sinkhole of collapsing demand—is what central bankers fear most of all.

When a deflationary collapse is severe enough—if the preceding bubble is large enough—it becomes a depression. In the 20th century a deflationary depression had happened only once; after the 1929 stock market crash in a devastating monetary cataclysm known as the Great Depression.

In the shell game of modern economics, credit replaces money and when credit gives rise

to speculative bubbles, the collapse of those bubbles leads to the defaulting of debt which

causes credit to disappear and the economy to collapse.

Schoon, The Shell Game, May 2008

http://www.investinganswers.com/financial-dictionary/economics/deflation-1160

In 2010, I wrote: Deflationary depressions occur after the collapse of large speculative bubbles. The collapse of the 1920s US stock market bubble, then the largest bubble in history, caused the Great Depression of the 1930s. The collapse of the far larger dot.com and US real estate bubbles will cause the next.

…The present economic crisis is similar to that of a patient who has suffered a massive near-fatal heart attack. Presently surviving only because of constant care and unprecedented levels of medication, it is the unprecedented levels of medication that will ultimately cause the patient’s death.

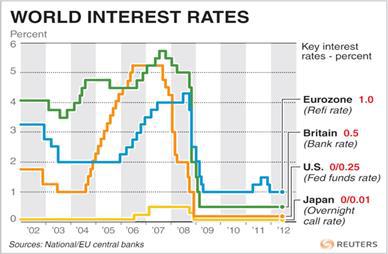

The amount of monetary stimulus keeping the global economy afloat has never been greater. Two of the largest economies in the world, the US and Japan, now have interest rates close to zero…

QUANTITATIVE EASING

The 2008 economic crisis was so severe central banks around the world were forced to slash interest rates to historic lows and began buying record amounts of government bonds to force rates lower to enable governments to borrow at far below market rates.

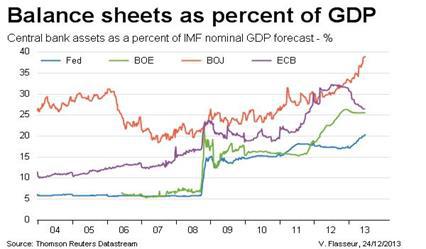

This is the raison d’être for central banks’ quantitative easing: As demand falls, central banks are buying unprecedented amounts of government debt in order to keep sufficient capital circulating in their increasingly sclerotic economies; and, as a result, central bank balance sheets are now filled with historic levels of increasingly suspect government debt.

The world’s central banks not only now own record amounts of government debt, the value of that debt—if marked-to-market—is significantly lower than nominally priced; and, if interest rates rise, central bank balance sheets could be wiped out resulting in the bankruptcy of central banks themselves.

Although the Fed does not value its portfolio on a mark-to-market basis, the spike in interest rates over the second quarter has already reduced the market value of the Fed’s portfolio by about $192 billion, wiping out the entirety of the past year’s unrealized portfolio gains. Higher rates would continue to reduce the value of liquid assets available for sale, thus eroding the Fed’s capital cushion. Given that the Fed’s capital currently sits at only $55 billion, a continued increase in interest rates could potentially erase the Fed’s capital base. This could impair the Fed’s ability to sell assets and protect the purchasing power of the dollar, which in turn could reduce the value of Treasuries and push interest rates even higher.

http://guggenheimpartners.com/perspectives/macroview/the-fed%E2%80%99s-balance-sheet

CENTRAL BANKS: DRINKING POISON TO CURE THIRST

Extreme measures of monetary stimulation via money printing are necessary to counteract the deflationary pressures set in motion by declining asset values against which massive amounts have been borrowed. But, in the end, creating money out of nothing will reduce the value of money to exactly that—nothing. This is the path upon which governments and central bankers have embarked. Fraught with danger and pitfalls, it was not their first choice—it was their only choice.

Schoon, 2010: Ready Or Not, Here It Comes, December 2009

By their excessive monetization of debt, QE etc., the Fed, the BOE, the ECB, BOJ and the PBOC are drinking poison to cure thirst; and, while they’re desperately hoping to restart their moribund economies, their attempts to do so may bring about what they’re trying to avoid—a catastrophic deflationary collapse.

Literally, trillions of dollars of Fed liquidity, QE1, QE2, QE3, combined with simultaneous and unprecedented monetary stimulation by the central banks of Europe, England, Japan and China have been required to offset the ultimately fatal decline in demand that occurs in the deflationary wake of large collapsing bubbles—and despite the unprecedented levels of quantitative easing by central banks, deflation is now gaining the upper hand.

Deflation, not inflation, is now the greatest concern for the world economy. Over the past year, producer prices have fallen throughout the advanced world; consumer prices have been falling for the last 6 months in France and Germany; in Japan wages have actually fallen 4 percent over the past year. Until the recent crisis prices were falling in Brazil; they continue to fall in China and Hong Kong; they will probably soon be falling in a number of other developing countries.

Paul Krugman, MIT blog

Ben Bernanke’s strategy of monetary easing is drawn directly from the playbook of Milton Friedman, Bernanke’s mentor at the University of Chicago. Friedman believed that sufficient expansion of the money supply, i.e. artificial inflation, during the 1930s would have overcome the deflationary forces responsible for the Great Depression.

Bernanke is following the monetarist depression-prevention model hatched by Nobel laureate and libertarian patron saint Milton Friedman. Bernanke has repeatedly invoked the late libertarian economist in support of lowering interest rates to zero, bailing out banks, and pumping untold trillions of dollars into the financial system. The implicit goal of these policies is to ignite artificial inflation.

By applying Friedman’s ivory tower solution, Bernanke and other central bankers contributed to the now extraordinarily high levels of government indebtedness which could trigger the very crisis central bankers are trying to avoid, i.e. another 1930s deflationary collapse.

On January 2, 2014, economists Carmen Reinhart and Kenneth Rogoff warned of this possibility in their paper presented to the American Economic Association:

The magnitude of the overall debt problem facing advanced economies today is difficult to overstate. . . . The current central government debt in advanced economies is approaching a two-century high-water mark…Delays in accepting that desperate times call for desperate measures keeps raising the odds that, as documented here, this crisis may in the end surpass in severity the depression of the 1930s in a large number of countries…

And at the same meeting of the American Economic Association, in response to questions from his peers (not from the media or the public), Ben Bernanke admitted the real goal of QE was to avoid deflation:

… the goal was to avoid deflation. So, one of our concerns, besides the weak recovery, at the time of QE2, was that inflation, as today, but even more so, was very soft and moving down. … we were concerned about deflation risks. Of course, deflation is not a zero [sum] thing. Even low inflation can create problems.

So, we adopted the quantitative easing policy with the objective of raising the inflation rate to meet our target; and at the same time, by doing so, of course, we would lower real interest rates and help the real economy.

Ben Bernanke: Deflation a concern before QE, CNBC January 3, 2014

Bernanke did not admit that Friedman’s solution had failed.

History will do that.

TIMING THE TIME OF THE VULTURE

In times of expansion, it is to the hare the prizes go. Quick, risk taking, and bold, his qualities are exactly suited to the times. In periods of contraction, the tortoise is favored. Slow and conservative, quick only to retract his vulnerable head and neck, his is the wisest bet when the slow and sure is preferable to the quick and easy.

Every so often, however, there comes a time when neither the hare nor the tortoise is the victor. This is when both the bear and the bull have been vanquished, when the pastures upon which the bull once grazed are long gone and the bear’s lair itself lies buried deep beneath the rubble of economic collapse.

This is the time of the vulture, for the vulture feeds neither upon the pastures of the bull nor the stored up wealth of the bear. The vulture feeds instead upon the blind ignorance and denial of the ostrich. The time of the vulture is at hand.

The above words ‘came’ to me in 1991. At the time, there were no signs of an impending economic collapse. Nonetheless, I began studying the Great Depression and by the end of the decade, when the dot.com bubble burst I was convinced another depression, a massive deflationary collapse, was on the way; except this time the severity of the collapse would be even greater because it would be accompanied by monetary chaos.

In the 1930s, the international monetary system was stabilized by gold because of the convertibility of paper money to gold. In 1971, however, the critical link between gold and paper money was severed as the US could no longer meet its obligations under Bretton-Woods. The consequences of that act of monetary apostasy are now in motion.

In 2006, I wrote in Time of the Vulture :

Because the US [over]spent all its gold and all currencies were anchored to gold through the dollar, all Central Bankers have been forced since the 1970s to participate in a confidence game they had not chosen of their own accord.

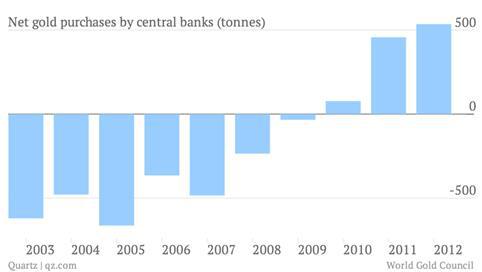

…Now, however, that is beginning to change. In 2006 many of the world’s Central Banks began to seek safer ground. Central Bankers are starting to look at gold in a new light… For two decades, Central Banks had helped the US Federal Reserve in stabilizing currencies by supporting paper money and suppressing gold. This has changed, as it is now understood that US spending and trade imbalances are the major threats to the world economy, not the price of gold.

The alliance of Central Banks supporting paper money against gold has dwindled considerably; but, more importantly, the Central Banks seeking to increase their gold reserves include the Central Banks of China, Russia, and the Middle East, all with large amounts of US dollars looking now to convert those dollars into gold.

I wrote those words in 2006 when central banks were net sellers of gold; and, in 2010, as I predicted, central banks instead became net buyers adding to the already growing global demand for gold.

In a free market, supply and demand dynamics would have sent gold soaring in 2013 as global demand for physical gold reached at all time highs. Instead, in 2013, the price of gold fell 28%, testament to the power of the bankers’ paper money to distort free market dynamics.

The bankers’ distortion of free markets began soon after the bankers’ introduction of debt-based paper money in 1694 resulting in economic expansion and contraction phases caused by credit and debt replacing supply and demand as primary economic principles.

Today, the bankers credit and debt ‘Ponzi Economy’ has become the global economic paradigm; indebting the world beyond its ability to pay except now by ‘ponzi-financing’, i.e. borrowing in order to borrow more. In 2010, I wrote:

Capitalism’s final stage is what [Hyman] Minsky calls “ponzi-financing”, when debt payments can only be made by additional borrowing. This is what the US, the UK and Japan are doing today, having to borrow against tomorrow in order to pay yesterday’s bills.

For 50 years, not one Dollar of new debt created by the US government to fund the activities it does not wish to tax for has been repaid. The debt has simply been “re-financed” with new debt being sold to retire the existing debt.

The Privateer, Late November 09, issue 6430100, www.the-privateer.com

At some point, the end finally arrives. Ponzi-financing cannot service debt forever. Investing in unhedged paper assets is the bet that it can. Gold is the bet that it cannot.

Schoon, 2010 Ready Or Not Here It Comes, 2010

CRUCIFIED ON A CROSS OF PAPER MONEY

Ponzi-financing is the final stage in the bankers’ 300-year old ponzi scheme. An extreme deflationary collapse is about to take away all what credit created and the take-away will not be easy for those attached to the world that is passing away.

The global economic collapse along with increasingly severe earth changes, e.g. record heat, record cold, earthquakes, drought, floods, etc., are the trigger events for a paradigm shift of cosmic proportions. The rebalancing of universal polarities is underway. A better world is coming.

In my youtube video, The End of the Beginning, Parts 1&2, I discuss the present and future stages of the collapse from a different economic perspective than in this article. See http://youtu.be/yRw5hA3DC_M.

On February 21/22, I will be speaking in Las Vegas at the Liberty Mastermind Symposium, February 21/22. For details see http://libertymastermind.us/ .

Buy gold, buy silver, have faith.

Darryl Robert Schoon

Pingback: New Zealand Almost Losing the Race to Debase | Gold Prices | Gold Investing Guide