We’ve learnt a thing or 2 in the past from Darryl Schoon. Both in person, having heard him speak and having had a couple of interesting conversations with him, but also in his writings. He has an ability to delve into history and pull a few new and interesting points out of the past that we’ve not heard before. So it is today. In this article he comments mainly on Central Bank “management” (a kind word for manipulation) of the price of gold, sharing some interesting writings on gold supply and demand, from someone we hadn’t come across before. He also covers:

1. The reasons behind Gordon Brown’s sale of much of the UK’s gold reserves.

2. His price estimate for gold without “Central Bank management”.

3. How the EFT’s GLD and SLV were used by central bankers to put a cap on golds rise last year.

4. And you won’t believe this, tracking the laughter of the members of the US Federal Reserve at the meetings and what it might indicate!!

Anyhow, there’s some interesting stuff contained, so read on…

GOLD FIRE SALE – Buy Now Sale Ends Soon

Inverse Lin-omena, the inverse of the Jeremy Lin phenomena where the unknown and previously discounted suddenly rise to prominence; here, the powerful and previously secure suddenly fall.

Today, central bankers, the mandarins of capitalism, are in disarray. Their attempts to contain capitalism’s current crisis increasingly resemble the tactics of a defeated army in retreat. Like Napoleon and Hitler’s respective “Moscow moments”, the 21st century economic crisis has brought to an end the bankers’ spectacular 300 year run at the table of power and wealth.

The indebting of others as a means of accumulating wealth ends when the indebted can no longer pay what they owe. The arcane and esoteric scribblings of second generation University of Chicago trained economists cannot cover up this basic fact, i.e. that the indebted are broke; and soon, their creditors will be as well.

The bankers’ franchise of credit and debt built on a leveraged foundation of paper money fractionally backed by gold allowed the West to accumulate geopolitical power and wealth on a vast scale. That era is now over.

It ended when the gold convertibility of the US dollar was terminated in 1971 when the cost of maintaining a global military presence outstripped the ability of the US to pay in gold what it owed on paper.

It was as if someone removed a pin from the axle of international commerce when the US dollar was no longer convertible to gold. Previously, the US dollar was linked to gold, and other currencies were linked to the dollar. Everything was stable. It is no longer so. Once the pin connecting gold and paper money was removed, everything changed. The axle of international commerce began to vibrate and lately it’s been getting much worse. The fear is that the wheels are now about to come off.

Section 1, topic 3, How to Survive the Crisis and Prosper in the Process, Schoon, 2007

Today’s fragile state of the euro, a fiat currency created in a failed European attempt to compete with and/or replace an increasingly unstable US dollar, is but another indicator that the wheels are now about to come off.

After the US ended the gold convertibility of the US dollar in 1971, gold skyrocketed from $35 per ounce to $850 in 9 years, increasing almost 2,500 % in value, dwarfing the later rise of the Dow (from 777 in 1983 to 11,722 in January 2000) a much smaller rise of 1,400 % over almost twice the time (17 years instead of 9).

After gold’s spectacular ascent, central bankers decided the price of gold needed to be ‘managed’, as a rapidly rising price of gold signaled that something was fundamentally amiss with the bankers’ fiat paper money, a signal that central bankers did not want sent, a signal that bankers would work exceedingly hard to disguise for the next 40 years.

When stocks lose their value

That’s a terrible thing

When homes lose their value

That’s a terrible thing

But when money loses its value

That’s the most terrible thing of all

– From: Introduction, How to Survive the Crisis and Prosper in the Process, Schoon, 2007

CENTRAL BANKERS MANAGE THE PRICE OF GOLD

In actuality, central bankers did not work ‘exceedingly hard’ to disguise the real market demand and price for gold. Instead, bankers disguised market demand not by hard work, but by smoke and mirrors, a contrivance common to confidence men everywhere and, today, to central bankers in particular.

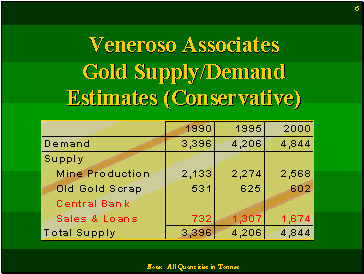

To suppress the price of gold, central bankers covertly supplied markets with gold bullion belonging to the nations on whose behalf they ostensibly toiled, suppressing gold’s real price with excess supply. This artifice was discovered by Frank AJ Veneroso, an extraordinary financial analyst and consultant well known only in the rarefied circles of international finance, see http://www.venerosoassociates.com/.

According to Veneroso, since the early 1980s central bank gold sales and loans comprised a significant portion of all gold sold. In 1990, Veneroso estimates that 21.5 % of gold sold that year came from central bank vaults; and by 2000, central bank gold sales had increased to over a 1/3 (34.6 %) of all gold sold.

Frank Veneroso’s story of central bank manipulation of gold markets is found at http://www.24hgold.com/english/contributor.aspx?article=1192026686G10020&contributor=Frank+Veneroso.

With thousands of tons of central bank gold coming onto the market, it’s clear why the price of gold declined from 1980 until 2001. What is remarkable, however, is that in the face of such overwhelming supplies, the price of gold began to rise in 2001.

THE TURNING POINT

The turning point, however, actually occurred in 1999 and is marked by an event relatively unknown and almost tantamount to financial treason. About that event, I wrote in March 2009:

In 1999, it was rumored that investment bank Goldman Sachs had a 1,000 ton gold short position in the markets. Goldman Sachs was betting that the price of gold would continue to fall and they would be amply rewarded for their apparent “risk”.

Because of central bank manipulation, the price of gold had moved inversely to the rise of stocks for almost 20 years and bankers were making easy money on the bet gold would continue its downward spiral.

However, much to the shock of Goldman Sachs and the central bankers, in 1999 gold stopped falling; and, because Goldman Sachs’ short position was so large, Goldman possibly could suffer catastrophic losses.

This is when England’s then Chancellor of the Exchequer, Gordon Brown, on May 8, 1999 announced England would sell over 50 % of its gold reserves, 415 tons of the most precious metal on earth at the very bottom of the market.

The decision to sell England’s gold thereby saved Goldman Sachs and insured the political future of Gordon Brown. Goldman Sachs’ is still in business and Gordon Brown is now [2009] the Prime Minister of England—proving that good things come to those who do the bidding of the powerful (whether either outcome was worth 415 tons of England’s gold is questionable).

Selling a nation’s gold to save the bankers’ parasitic system is now common practice as the banker’s system continues to collapse and gold continues to rise. Since Gordon Brown sold England’s gold, gold has risen from $275 dollars per ounce to its present price of over $900 despite the thousands of tons of central bank gold sold to prevent its inexorable movement higher. On 2/14/12 gold is $1,715]

CENTRAL BANK SALES AND LEASING OF GOLD HAS MADE GOLD AVAILABLE AT FAR BELOW MARKET RATES

To hide their burning house of cards, central bankers have sold thousands of tons of gold from national treasuries, mainly Switzerland, to keep the price of gold below what it would otherwise be. This is the true upside (for buyers) of the bankers’ gold suppression scheme.

While citizens cannot prevent central bankers from selling gold from their national vaults, today they are afforded the extraordinary opportunity to buy that very same gold on the open market at prices heavily discounted to their otherwise true market value.

My current estimate of today’s true market value of gold—without central bank intervention—is in excess of $10,000 dollars per ounce.

Many central banks, however, are today switching sides in the war on gold, preferring to keep their precious metals instead of selling them in an increasingly futile attempt to prevent the inevitable from happening—the collapse of the bankers’ now burning house of cards.

Today, the bankers’ fiat currencies are in a death spiral. It’s only a matter of time until the US dollar, the Japanese yen, the British pound and all paper currencies—including the Chinese yuan—come under the same pressure that now plagues the faltering euro.

Central bankers, however, will do everything in their considerable power to prevent their lucrative franchise of credit and debt based on paper money from collapsing; and, of late, they’ve discovered a new way to suppress gold and silver—the precious metal inventories of GLD and SLV, the precious metal ETFs used by investors to participate in the rising price of gold and silver.

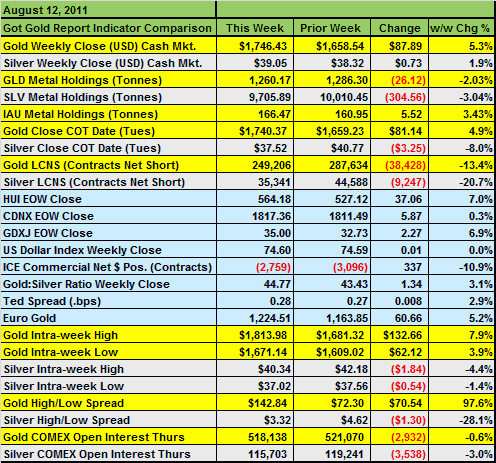

When Europe’s debt contagion spread in the summer of 2011, the price of gold began moving rapidly higher which bankers feared could itself turn into runaway contagion. The below chart shows that GLD and SLV, the ETF funds, were used by central bankers to cap gold and silver prices in mid-August.

http://www.gotgoldreport.com/2011/08/comex-swap-dealers-cover-gold-shorts-like-a-big-dog.html

Amid growing concerns about Europe’s debt crisis as gold rapidly rose, GLD sold 26.12 tonnes of gold and SLV sold 304 tonnes of silver, driving the price of silver down 8 % although gold rose 4.9 % despite GLD’s considerable efforts to the contrary.

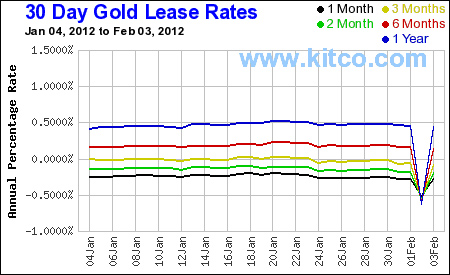

That GLD and SLV ostensibly dedicated to profit from the rising price of gold and silver would sell their inventories in a rapidly rising market runs counter to their mandate; unless, of course, they did so knowing that central banks would soon ambush gold and silver with deeply discounted lease rates on precious metals that would cut short gold’s increasingly spectacular rise.

Jesse’s Café Americain traces the planned ambush of gold by central banks during their September take-down, see http://jessescrossroadscafe.blogspot.com/2011/09/interesting-series-of-events-at-end-of.html. Gold had risen to a record high, $1900, on September 1st and on September 2nd, central banks then took corrective action, dropping their lease rates for gold sharply lower into negative territory.

This meant that central bankers would actually pay bullion banks to borrow their gold and sell it on the open market. The new supplies of gold capped gold’s increasingly steep seven month rise and, by the end of September, the price of gold fell back to $1600.

After Sept 2nd, gold lease rates still remained negative, insuring a continued low price for gold even as the European debt crisis accelerated and the global economy slowed. This is exactly what central bankers intended. Gold is a barometer of systemic distress and central bankers wanted to conceal the flames rising from their now burning house.

Nonetheless, even with negative lease rates, gold again began moving higher before central banks on February 2nd supplied markets with more gold with again sharply lower lease rates deep in negative territory.

As the bankers’ ponzi-scheme of credit and debt disassembles, central bankers will find it more difficult to contain the price of gold; and when gold does break out—as it will—the price of gold will exceed the $10,000 price it would now command if it were not for central bank intervention.

At $1700 gold is cheap; at $3,000 gold is cheap; at $5,000 gold is cheap; at $7,000 gold is cheap. Wait till the central bank sale ends and you will realize how cheap gold actually is.

The wheels are now coming off the bankers’ once invincible juggernaut. Whether the out-of-control bankers will crash in a (1) hyperinflationary blow-off, (2) a brutal never-ending deflationary collapse-in-demand or (3) in a fatal bursting of capitalism’s bloated colostomy bag—derivatives—cannot be known.

But what is known is that the end of the bankers’ monetary fraud is near and its demise closer than most want to believe.

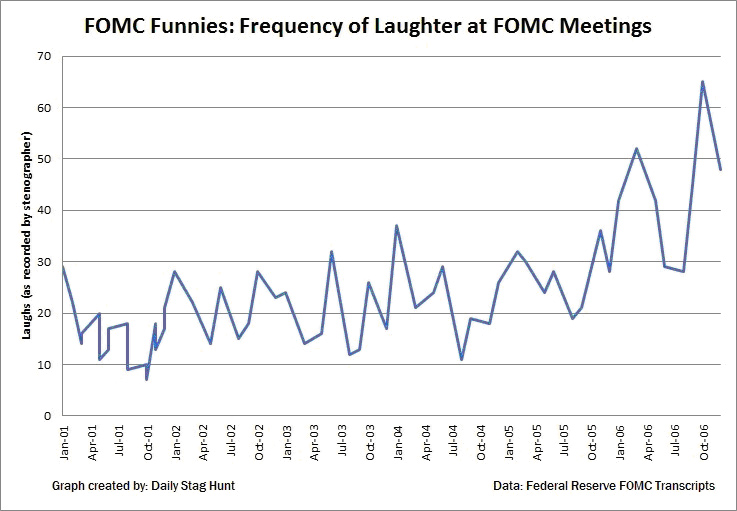

THEY’RE NOT LAUGHING ANYMORE

A remarkable blog, www.dailystaghunt.com, reviewed recordings of Fed Open Market Committee meetings between 2000 and 2006 and, interestingly, noted the frequency of laughter during meetings, observing: The number of recorded laughs actually increased in frequency from 2000 to 2006. In 2001, the FOMC erupted into laughter 16.5 times per meeting on average. In 2003, it was over 19. In 2005, 27. And then in 2006, the FOMC burst into laughter nearly 44 times per meeting!

As the 2007/2008 financial crisis grew closer, central bankers grew increasingly relaxed and confident; believing their extremely low 1 % interest rates had worked; that they had survived the collapse of the greatest speculative bubble in the US since the 1920s—the collapse of the 2000 dot.com bubble—and all was well.

But those in attendance, Greenspan, Bernanke, Fisher, Mishkin, Krozner et. al., were wrong. Their fatally flawed solution to the collapse of the dot.com bubble, low 1 % interest rates, had given birth to an even more dangerous bubble, the 2002-2006 US real estate bubble, the largest speculative bubble in the world whose collapse would bring down the world economy in 2007/2008.

Of course, this wasn’t known in 2006. In 2006, central bankers were still laughing.

Frequency of laughter during FOMC meetings

Year Average laughs per meeting

2000 16.5

2001 15.375

2002 21.625

2003 19.25

2004 23.125

2005 27.25

2006 43.875

Data on the frequency of laughter at FOMC meetings after 2006 is not yet available. But it can be assumed the frequency subsided after the massive global credit contraction in August 2007 and after the collapse of world markets in 2008.

Note: the possibility that FOMC laughter remained high or actually increased after 2006 is far too macabre to consider. We do, however, await additional data before passing judgment.

http://www.dailystaghunt.com/markets/2012/1/12/the-correlation-of-laughter-at-fomc-meetings.html

Today, central bankers are no longer laughing. Their nights are considerably longer as are their weekends; their daily grocery list might now include quarts of gin and whiskey, prescription anti-depressants and extra-strength deodorant.

We are collectively in the end game, a period of great change where the present paradigm is collapsing making way for what is to come. Keep your thoughts positive and focused on what is coming, not the troubled passing of the present world. Let central bankers do that.

Note #1: I will be speaking at Professor Antal Fekete’s New School of Austrian Economics in Munich, Germany, see http://www.professorfekete.com/gsul.asp . For details, contact nasoe@kt-solutions.de

Note #2: My latest video, What and Who Do Bankers Do (or what I really think about bankers and money). Dollars & Sense show #12, http://youtu.be/hazULFo3oB4

Buy gold, buy silver, have faith.

Darryl Robert Schoon

Blog www.posdev.net/pdn/index.php?option=com_myblog&blogger=drs&Itemid=81

Pingback: Chart of the week: Gold in NZ dollars ready to break out? | Gold Prices | Gold Investing Guide