Darryl Schoon is back with another history lesson. This time looking at gold from 1870 right through to the early 2000’s…

The Price of Gold and the Art of War Part I

If you wait by the river long enough, the bodies of your enemies will float by

Sun Tzu, The Art of War, Fifth century BC

Only fools and the ideologically impaired believe that today’s capital markets are free. In free markets, prices are determined by supply and demand. In capital markets, supply and demand considerations are subordinated to capitalism’s increasingly dysfunctional monetary menses, i.e. credit flows, emanating from central banks. Of all markets, today’s gold markets are the least free.

For almost three centuries, gold played a critical role in the bankers’ extraordinarily successful scheme to defraud society by substituting debt-based money in place of savings-based money, silver and gold, by introducing otherwise suspect paper money into circulation via the ubiquitous mechanism of credit so as to profitably skim societal productivity, entrepreneurial ingenuity and constantly increasing government expenditures via constantly compounding interest.

In the early 20th century, a negative trade balance beginning in the 1870s exacerbated by the overhead of an aging empire beset by nationalist insurgencies and the military costs of preparing for WWI, forced England to share the care and feeding of its golden goose, capitalism, with its former colony, the United States of America.

This was done in 1913 by the creation of a carbon copy of its central bank, the Bank of England, in the US with the enactment of the Federal Reserve Act. The reason given was that the establishment of a central bank in the US would prevent financial crises from occurring in the future as they had in the past.

The Federal Reserve System (also known as the Federal Reserve, and informally as the Fed) is the central banking system of the United States. It was created on December 23, 1913, with the enactment of the Federal Reserve Act, largely in response to a series of financial panics, particularly a severe panic in 1907.

http://en.wikipedia.org/wiki/Federal_Reserve_System

Only two decades later, the Fed’s loose credit policies resulted in the speculative excesses of the 1920s, i.e. the ‘roaring twenties’, and the subsequent 1929 collapse of the New York Stock Exchange which plunged the US into the Great Depression of the 1930s—a crisis which made the financial panic of 1907 look like a mild case of neurasthenia.

But after the greatest crisis in the history of capitalism—a crisis the Federal Reserve Act was allegedly designed to prevent—there was no debate to revoke the charter of the Federal Reserve. This is because the reason for the Fed’s existence, i.e. to prevent future financial crises, was a smokescreen to hide a far more insidious agenda.

DEBT-BASED MAMMON AND THE FALL OF AMERICA

The purpose of central banks such as the Federal Reserve is not to prevent financial crises or to ensure price stability or even today’s mandate of the moment, to promote full employment. These are canards raised by central bank/Fed toadies in their craven defense of the bankers’ long-running and immensely profitable predatory ponzi-scheme.

The purpose of the Federal Reserve and all central banks is and has always been to benefit bankers by indebting nations, allowing bankers and the favored few to live off the constantly compounding interest of said indebting ad infinitum. In this, the Federal Reserve has succeeded beyond all previous measures of success.

AMERICA SPENDS THE BANKERS’ GOLD, PAPER MONEY LOSES ITS INTRINSIC VALUE AND TRIGGERS CAPITALISM’S END GAME

The Fed’s care and feeding of England’s golden goose, i.e. capitalism, almost resulted in the complete collapse of capital markets in the 1930s. However, extending the franchise of central banking to America would do far worse. America’s military spending after WWII would cost central bankers the gold required to pass off their paper banknotes as money.

In 1949, the US possessed 21,775 tons of gold which backed the US dollar, stabilized capital markets and constrained the ability of governments to print excessive amounts of paper money. But, after 1949, unprecedented levels of US overseas military spending and the costly overseas expansion of US multinational corporations drained the US Treasury of so much gold the US could no longer redeem the flood of US dollars circulating overseas.

In August 1971, at the urging of Paul Volker, then Under-Secretary of the Treasury, President Nixon ended the convertibility of the dollar to gold; and for the first time in history gold was no longer money.

Although gold and silver are not by nature money, money is by nature gold and silver

Karl Marx, Das Kapital – Volume 1, Chapter 2

Because all paper currencies were pegged to the US dollar and the US dollar was convertible to gold, all currencies lost their connection to gold when the ties between gold and the dollar were cut. As a consequence, on August 15, 1971, all currencies in the world became fiat.

Paul Volker took full responsibility for triggering capitalism’s end game. In a 2013 interview, Volker explained his role in that consequential act with more than a modicum of pride: I certainly was a major proponent of suspending gold convertibility, in fact the principal planner.

PRIDE GOETH BEFORE A COMING FALL

Because of Volker’s actions, only the full faith and credit of soon-to-be bankrupt nations now guaranteed the value of constantly deflating currencies issued by central banks; and the role of gold shifted from guaranteeing and stabilizing the value of the bankers’ paper banknotes to becoming the competitor of paper money itself—for the declining value of fiat paper money could now be directly measured by its declining worth against the price of gold.

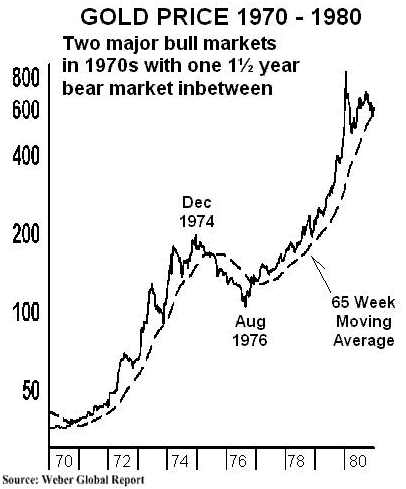

When ties between gold and the dollar were cut, gold rose from $35 on August 15, 1971 to $197.50 by December 30, 1974. The 560 % rise in only 40 months was exactly what central bankers feared; as the world watched, the value of the bankers’ paper money was rapidly depreciating against gold.

The bankers had to act quickly and they did. In December 1974, the US intervened. Between December 1974 and August 1976, the price of gold plunged, falling from $197.50 to $103.50, a 47 % decline.

In Topic 13 in Time of the Vulture, I described how the US forced gold lower:

…in December 1974 [the US government] announced it would be selling two million ounces of gold. The price of gold, which had begun to rise after being de-linked from the US dollar, fell on the news that a large supply was soon to be available. This was exactly what the US government wanted.

…Next, in 1975 the International Monetary Fund, which has often functioned as an extension of the US, announced it would sell 25 million ounces of its gold. These two announcements alone would have been more than enough to drive the price of gold significantly lower except for one not-insignificant detail—at the exact same time, US inflation rates began spiraling out of control.

From 1976 to 1980, US inflation increased from 5.22 % to 13.91 % and the price of gold responded accordingly; skyrocketing from $102 per ounce in 1976 to $850 in 1980. Instead of forcing gold down, the market absorbed all the gold the US and IMF sold and then some. This is a lesson that bears remembering because gold will soon again experience a meteoric rise in spite of government attempts to the contrary.

DRSchoon, Time of the Vulture: How to Survive the Crisis and Prosper in the Process, May 2007

THE WAR ON GOLD

Years of study have convinced me that there is a strong and criminal agenda to illegally suppress the price of gold.

Ferdinand Lips (Managing Director of Rothschild Bank, Zurich), 2001

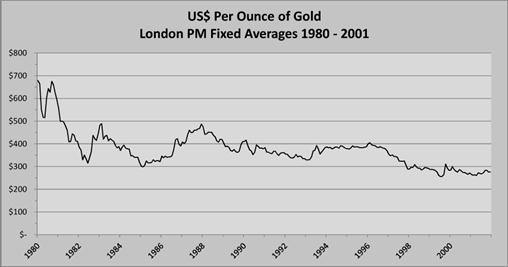

Despite unprecedented levels of credit creation and money printing by governments, over the next 20 years the price of gold would fall 70 % as central bankers flooded markets with leased central bank gold forcing gold lower.

In Topics 17/ 18 in Time of the Vulture, I described how central banks colluded with investment banks to accomplish their ends:

In 1998…the price of gold was hovering between $280 and $300 per ounce, lower than at any time during the previous twenty years… collusion between Central Banks and investment banks had finally forced down the “free-market” price of gold.

In so doing, investment banks had convinced the Central Banks that they had a better use for Central Bank gold. And they did. At least it was better for the investment banks. It was also to be the last time the Central Bankers were to see their gold.

…[In the 1990s] the annual demand for gold was 4000 tonnes (metric tons) per year. Since gold mining produces around 2500 tonnes yearly, there is an annual shortfall in production of 1500 tonnes, 60% of production.

If grain harvests were continually short of demand by 60%, grain prices would be skyrocketing and those holding grain would be trying to take advantage of this shortfall to make windfall profits; loaves of bread would be getting smaller and smaller and their cost increasingly dear. But this was not grain, it was gold.

The speculative frenzy surrounding gold should have been spectacular. But it wasn’t. There were no spectacular profits in the making on gold’s explosive upswing because there was no upswing.

…Beginning in the 1980s, the US Fed and other Central Banks started to loan out their gold reserves to investment banks at the very low interest rate of 1%. The investment banks would sell the gold, investing the proceeds in interest-bearing bonds paying higher, for example, 6% interest. The 5% spread between interest rates was their profit.

This continual new supply of gold on the market forced gold prices lower over time, which is what both the Central Banks and investment banks wanted. The Central Banks wanted gold lower because it made inflation less visible and their paper currencies appear more stable. The investment banks wanted gold lower because when it came time to repay their gold loans they could buy gold at a lower price and make even more money.

This became known as the gold-carry trade, a forerunner of the Japanese yen-carry trade that was to come later. In both instances the original asset (gold or yen) would be borrowed at low interest (1% for gold, 0 % for yen) and would be sold, with the proceeds reinvested in assets that offered higher rates of return.

The only risk was that if the underlying asset (gold or yen) rose in price before the time came due to repay the loan, the underlying asset would have to be purchased at a higher price, incurring perhaps serious losses for the borrower. This risk was later to become more than just apparent.

As long as prices stayed low, the gold carry-trade was a win for the Central Banks wanting to suppress the price of gold and the investment banks that were handsomely profiting once more at the trough of government largesse.

The extent of these gold loans was hidden, as the Central Banks did not want known the level of their collusion in the illegal manipulation of gold markets; and if it weren’t for the efforts of [noted investment advisor/analyst] Frank AJ Veneroso, the real volume of gold loans would never have been discovered.

… Veneroso discovered that the Central Banks were hiding the vast majority of their gold loans from public view… Ten to fifteen thousand tonnes of gold, an amount far larger than the Central Banks would admit, had been loaned to the investment banks in order to suppress the price of gold and now, in Veneroso’s opinion, were never coming back.

In 1999, however, the gold-carry trade came to a halt when gold’s 20-year descent ended. The investment banks, however, had literally ‘bet the bank’ on falling gold prices and found themselves on the edge of bankruptcy should the price of gold rise.

The underlying asset of the carry-trade, i.e. gold, had stopped falling and the banks’ highly leveraged bets now exposed them to massive losses on a scale that threatened the very foundation of banking. What happened next reveals the symbiotic link between banking and government. It also explains why governments used taxpayer money to rescue Wall Street in 2008 to keep that link intact; because without banks, today’s governments would fall.

Governments and banks are a two-headed hydra and each needs the other to survive. Governments need banks to borrow and lend and banks need governments to legitimize the banks’ creation of money that previously did not exist.

TODAY’S

TODAY’S

TWO-HEADED HYDRA

CENTRAL BANKS

AND GOVERNMENTS

Image: http://en.chessbase.com/post/nine-headed-monster-wins-paderborn

THE 1999 GOLD CRISIS

In 1999, the twenty year descent of gold ended. By then, Wall Street bets on a falling gold price were so large if gold prices rose, the losses would wipe out the net worth of at least one, if not two of the largest investment banks in the world putting the infrastructure of the financial world at risk.

We looked into the abyss if the gold price rose further. A further rise would have taken down one or several trading houses, which might have taken down all the rest in their wake. Therefore at any price, at any cost, the central banks had to quell the gold price, manage it. It was very difficult to get the gold price under control but we have now succeeded. The US Fed was very active in getting the gold price down. So was the U.K.

— Eddie George, Governor Bank of England, in a conversation with Nicholas J. Morrell, CEO of Lonmin, September 1999

The 1999 gold crisis is discussed in the 2007 edition of Time of the Vulture. Because fractional reserve banking is a con game wherein confidence is paramount, governments and bankers’ did not want either the crisis known or its cause revealed so speculation and rumor existed in place of fact. In 2012, however, the cause of the 1999 crisis was substantiated in the media and was included in my 2012 update of Time of the Vulture.

I planned to do a 2014 edition but instead decided to offer the 2012 edition at a lower price. Written in 2006/2007, my predictions are as true today as they were then. The bankers’ war on gold is still in progress and as is the predicted deflationary collapse that is being played out today on the world stage.

In my next article, The War On Gold And The Art Of War, Part II, I will discuss gold’s rise from its $252 low in 1999 to its high at $1900 in 2011 and its temporary fall to $1255. Along with the bankers, the biggest losers in the war on gold will be those who are unaware a war is being waged.

As I wrote in Time of the Vulture: … the vulture feeds neither upon the pastures of the bull nor the stored up wealth of the bear. The vulture feeds instead upon the blind ignorance and denial of the ostrich. The time of the vulture is at hand.

On Sept. 29, 30 and 31st, Time of the Vulturewill be available at a special low promotion price. Go to the bookstore page at drschoon.com. For those outside the US, go to amazon.com. My current youtube video, Stories the US and CIA Don’t Want Told, Part I, is inspired by the life and death of Gary Webb, the award winning journalist.

The end is near. So is the beginning.

Buy gold, buy silver, have faith.

Darryl Robert Schoon

Pingback: THE PRICE OF GOLD AND THE ART OF WAR Part II - Gold Prices | Gold Investing Guide