Bank runs might seem like a far fetched possibility, both in the USA and here in New Zealand. But the below article shows just how little physical paper currency there is available in the USA compared to the total dollars in US cheque and savings accounts.

It inspired us to have bit of a dig around to see what the numbers were in New Zealand in terms of paper money in circulation versus bank deposits. Here’s what we found…

New Zealand Paper Money in Circulation vs Bank Deposits

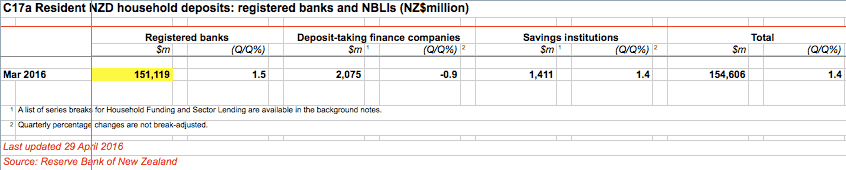

As of March 2016:

NZ Household Deposits with NZ Registered Banks totalled $151.1 Billion.

(We didn’t worry about including the Deposit-taking finance companies and the Non Bank Lending Institutions as they only added another couple billion dollars. And these days what’s a couple billion dollars?!)

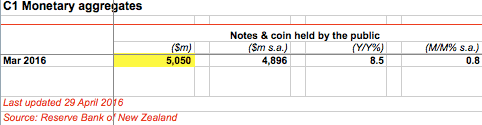

While the total notes and coin held by the public was $5.05 Billion.

However we had trouble finding the number for the total notes and coin that are held by banks as of March 2016. (This figure is not itemised out of the M1, M2 and M3 data we found above).

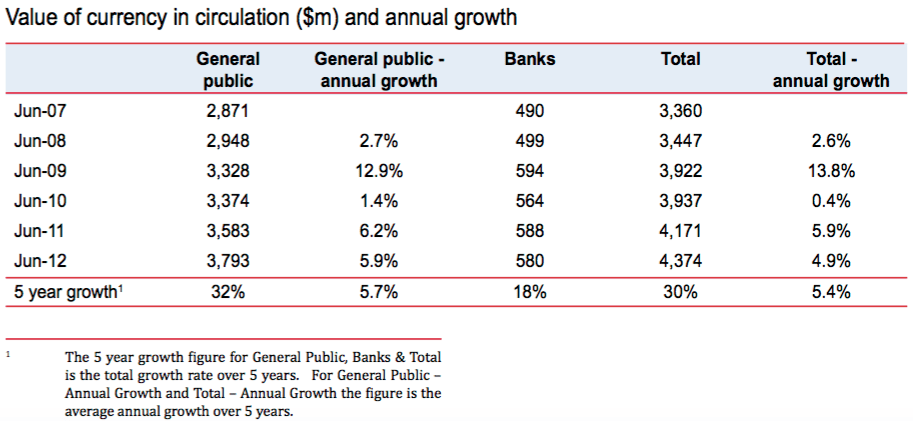

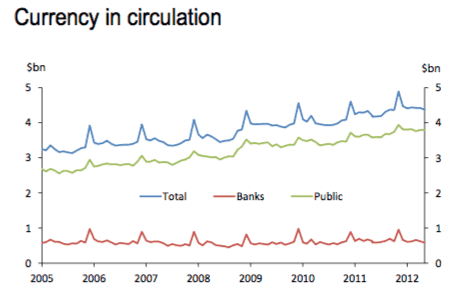

But we looked back to the last time we found this figure referenced which was in June 2012 in a RBNZ document: “Recent trends and developments in currency 2011/2012”

That was a figure of $3.79 Billion held by the public and $0.58 Billion by banks. For a total currency in circulation of $4.37 Billion. See the far bottom right of the below table.

While back in 2012 total household deposits with Registered Banks totalled $106 Billion. Source.

So this was a big difference:

$4.37 Billion in Paper money in circulation versus $106 Billion in Deposits.

Obviously this figured has changed since 2012. Deposits have increased from $106 Billion to $151 Billion as of March 2016. A big jump.

While currency in circulation held by the public has increased from $3.79 Billion to $5.05 Billion.

The below chart shows that the notes and coins held by Banks remained very stable from 2005 to 2012. So odds are that the paper money held by the banks hasn’t changed dramatically from 2012 to 2016 either.

So what if a portion of the New Zealand public decide they want to remove their deposits from the banks and take the cash instead?

This data clearly shows how little physical currency in the form of New Zealand notes and coins is on hand. In 2012 the public already held 87% of the physical cash, with banks only holding the remaining 13%. As noted already the total notes and coins the banks held didn’t really change from 2005 to 2012. So odds are this percentage may actually now be even lower as the notes and coins held by the public has increased over the past 4 years.

While a bank run in New Zealand may not appear to be a risk right now, we are seeing negative interest rates becoming more and more common the world over. Japan has them and has seen an increase in the sales of safes. Why is that?

Instead of the negative interest rates forcing people to spend like the central bankers hoped, people are choosing to withdraw physical cash from the banks and hold it at home.

Negative interest rates aren’t here in New Zealand, but it is worth considering the ramifications if they were to be implemented down the track.

In case you didn’t already know, there is no government guarantee of bank deposits in New Zealand. So were bank runs and bank failures to occur, as a deposit holder you face the risk of a “hair cut” on your savings. [Learn more about this here: RBNZ Bank “Bail In” Scheme for Bank Failures: The Open Bank Resolution (OBR)]

As part of a financial insurance preparation for such an occurrence, the below article recommends an allocation of 10-15% to gold and silver, along with a “stash” of physical cash. Read on for more about that…

Coming Bank Run Will Send Gold to $3,000+

By Dan Steinhart

Editor’s note: Today, we’re changing up our normal Dispatch schedule to bring you an extremely important warning. This could be one of the biggest threats you face today…and the likelihood of it happening has never been higher. (And make sure to read until the end… We have an incredible offer for you that closes tonight.)

You’re alone in a foreign country, far from your hotel.

You reach in your pocket to grab your wallet. It’s gone…

All your cash, credit cards, and debit cards are in it.

You can’t buy food…or a cab ride…or anything.

You try not to panic. What will you do?

This feeling, multiplied by 1,000, is what a bank run feels like.

A bank run is when banks run out of cash. It’s when too many folks try to pull their money out at the same time, and banks shut down. No one can access their cash.

Not many folks know this, but we came within hours of having a full-scale bank run in the U.S. during the financial crisis in 2008.

Customers pulled $5 billion of cash out of failing bank Wachovia, once the fourth largest bank in the U.S. This pushed it to the brink of collapse. The U.S. government bailed it out over a weekend, at the last second.

Carlos Evans, a Wachovia executive, said Wachovia went from “OK” to “in trouble” in less than a week.

He said “I don’t think people understand how quickly events unfolded.”

In this essay, I’ll explain why a real bank run could easily happen in the U.S. within the next two years.

And, if you don’t get money out beforehand, it will be trapped in the closed bank.

Folks who understand how this disaster will play out can sidestep it. You’ll even have a chance to make 200%+ gains because of it, as I’ll explain in a moment.

I know I’ll get angry emails for writing about this topic. Folks will point out that a major bank run hasn’t happened in the U.S. since the 1930s. They’ll say that a bank run in the U.S. is a one-in-a-million shot. They’ll call us fearmongers for even talking about such a catastrophic event.

I agree that a bank run would be catastrophic. It would blindside 999 out of 1,000 Americans. It would leave many Americans who keep all their money in the bank without a dollar to buy food or gas or medical care.

But unfortunately, I think most folks are vastly underestimating the likelihood of a bank run. The odds of one have risen dramatically since the 2008 financial crisis.

We are in much more danger of a bank run today than at any point since the Great Depression.

Why do I say that?

It’s not because banks don’t have enough money in their vaults—even though that’s true. These days, if even 1 in 10 customers tried to withdraw her money from the average bank, it would have to shut down.

But that’s not the reason why a bank run is highly likely in the next two years…

The Reason Is Negative Interest Rates

You’ve likely heard of negative interest rates by now. They’ve been all over the news.

In short, negative interest rates turn your savings account upside down. In a normal world, your bank pays you interest on your savings. It takes your money, pools it with other people’s money, and loans it out.

The bank makes money by paying out less in interest on your deposit than it earns in interest from borrowers.

This is how it has worked for decades.

Negative interest rates flip this on its head. Instead of earning interest, the government orders banks to charge you interest on your own money.

Negative interest rates could only exist in a crazy world where idiot politicians are in control.

Unfortunately, that’s just what we’re dealing with right now.

Politicians all over the world are ordering banks to charge you a fee for storing cash.

The Bank Account Tax

And the more cash you have, the more you pay in fees. We’ve called this the “bank account tax.” And it will likely lead to millions of folks pulling their money out of the bank to avoid paying the tax.

You see, government bureaucrats think that taxing your bank account will get you to save less and spend more money. This would lead to people buying more things like TVs, cars, and stocks.

This would “stimulate” the economy.

This thinking is dead wrong.

Negative interest rates won’t get folks to spend their hard-earned savings. Although mainstream economists claim spending drives the economy, many Americans instinctively know better. They’re not going to stop saving for retirement or for their kid’s college.

Instead, they’ll pull their cash out of the bank and put it in a safe or under their mattress. Folks will hoard money at home, where negative interest rates can’t tax their savings to death.

This is already happening in Japan, where the key interest rate is negative. Folks are pulling cash out of banks and locking it up in safes at home, causing an explosion in safe sales.

And here’s the thing…

It would only take a small fraction of withdrawals in the U.S. to force the banking system to shut down.

Here’s a little-known fact about the U.S. financial system. If you add up all the cash sitting in Americans’ checking and savings accounts, you get $11.1 trillion.

But according to the Federal Reserve, there are only about 1.4 trillion “paper” dollars in circulation in the U.S.

As you can see in the chart below, there are nowhere near enough “real” dollars in the system.

If even 15% of depositors tried to take their cash out of the bank, the banking system would collapse. Banks would be forced to shut down, locking you out of your account.

In normal times, this lack of dollars isn’t an issue. Less than 1% of folks try to withdraw large sums of cash each day. So banks can get away with having hardly any real physical cash.

But these are not normal times.

Remember, governments are ordering banks to tax your bank account with negative interest rates.

This has never, ever happened before. Not in the U.S. or anywhere else.

But it is happening all around the world right now. Key interest rates in Japan and Europe are already negative. And Janet Yellen, head of the Federal Reserve, recently said negative interest rates aren’t “off the table” in the U.S.

Your 3-Step Protection Plan

So, how can you protect yourself from this lunacy?

Well, at a minimum, you should have an emergency backup plan in the event of a bank run. We recommend keeping enough cash in your home to live on for at least three months. Six months’ cash is even better.

You can keep the cash in a safe hidden in your house. Or you can bury it in your backyard in an airtight, waterproof container. PVC pipes work well for this. You can buy them at Home Depot.

You should also own lots of physical gold and silver. As a general rule, we recommend having 10%-15% of your investable assets in physical gold and silver.

Gold and silver have served as money for centuries. They’ve outlived bank runs…hyperinflations…and every other kind of financial crisis.

Gold is the ultimate currency because it doesn’t rot or corrode…it is durable…easily divisible, portable, has intrinsic value, is consistent around the world…and it cannot be created from thin air. It cannot be debased by the government.

That last part is extremely important. As you likely know, governments often do reckless, destructive things during times of financial trouble.

How do you think the government would react to the ultimate financial crisis…a bank run that locks Americans out of their own bank accounts?

There’s no way to know for sure. But if you’re familiar with the reckless policy of “quantitative easing,” you know the government has created 3.5 trillion new dollars from thin air since the 2008 financial crisis.

You can bet the government will not hesitate to create trillions more dollars during a cash shortage.

And, as basic economics teaches us, creating new dollars destroys the value of the dollars in your bank account.

I expect this to create a “mad scramble” for physical gold and silver. This will cause their value to skyrocket.

Right now, probably less than 1% of Americans own a single gold or silver coin. If that number rises to just 2%, it would create a huge swell of demand for gold. It could easily push gold prices to $3,000 and beyond. And it could easily push silver prices to $35 and beyond.

Keep in mind, these are conservative estimates. Casey Research founder Doug Casey expects gold to hit $10,000/oz. Many well-known analysts agree with him. Jim Rickards, gold expert and former CIA insider, also expects gold to hit $10,000. So does Porter Stansberry, who’s famous for predicting the 2008 mortgage crisis and the demise of fraudulent companies Fannie Mae and Freddie Mac.

Despite all the evidence I’ve showed you, I know some of you will refuse to believe a major bank run could happen in the U.S.

Just remember, citizens of Greece thought the same thing before its banking system collapsed last year. As you may have heard in the news, Greek banks closed for 20 straight days. Many folks couldn’t buy basics like food or medical care.

And keep in mind, Greece isn’t a third-world country. It’s a member of the European Union with rich countries like Germany and France. And it uses the euro, the second most important currency in the world.

As I explained, you should take two critical steps to protect your money from a bank run. After you’ve taken step 1 (keep cash at home) and step 2 (own physical gold and silver), you may also want to play “offense” by owning gold stocks.

While gold is up 21% this year, gold stocks are up more than 70%. This is possible because gold stocks often offer 3x, 4x, or 5x leverage to the price of gold. So if gold goes up 100%+ like we expect, gold stocks could easily gain an average of 300%, 400%, or 500%.

And the very best gold stocks could gain 1,000%, 2,000%, or more. We saw this happen during the last gold bull market, when the average gold stock gained 602%.

In short, we have an extremely rare opportunity to make “10-bagger” gains in gold stocks right now. Doug Casey recently invested $800,000 of his own money into gold stocks for this very reason.

We want as many people as possible to profit from this opportunity. That’s why we’re offering a special $500 discount on International Speculator. In this gold stock research service, Editor Louis James shares the very best gold stocks to buy right now. But you’ll have to act quickly. This offer expires tonight at midnight.

When you sign up, you’ll get instant access to our new special report: “9 Essential Gold Stocks to Buy Now.” You’ll also be enrolled in a trial membership, which gives you the right to try out this service risk-free for 90 days.

But remember, today is the LAST DAY we’re offering this discount. And with gold prices surging, the window of opportunity to buy gold stocks could slam shut at any time. Once it closes, we likely won’t get another chance like this for years. Learn more here.

Regards,

Dan Steinhart

Delray Beach, Florida

May 6, 2016

Good article. I looked into this data a few months ago myself. As the true definition of inflation is “the increase of the money supply” What I’m wanting to know is where is the inflation hiding and what will it take to bring it out? Cheers

Yes indeed that is the 64 trillion Dollar question! So far most of this extra money is sitting as excess reserves with the Central Banks as the banks haven’t loaned much of it – maybe because there hasn’t been sufficient demand. Perhaps it will take actual helicopter money where the governments spend the printed money themselves to really get it sloshing around the global economy? Jim Rickards outlines this in something we just posted: https://goldsurvivalguide.co.nz/the-elites-plan-for-global-inflation-part-ii/