Gold and interest rates are often described as moving in opposite directions.

The common belief is simple:

- Rising interest rates are bad for gold

- Falling interest rates are good for gold

At first glance, this makes sense.

Gold does not pay interest or dividends. So when interest rates rise, savings accounts and bonds begin offering higher returns. That can make gold appear less attractive.

But history shows the relationship is not that straightforward.

Gold has sometimes fallen while rates were rising. In other periods it has risen alongside higher rates.

So what actually matters?

In this guide we’ll look at:

- Why many people think higher rates hurt gold

- Why interest rates alone do not tell the full story

- What previous rate cycles can teach us

- Why gold sometimes rises alongside higher rates

- What rising rates may mean today

Table of Contents

Estimated reading time: 7 minutes

Why Many People Think Rising Interest Rates Hurt Gold

The idea that rising rates are bad for gold usually comes back to one word:

Opportunity cost.

Gold does not generate income.

A bank term deposit, savings account or government bond may pay interest.

So if interest rates move from 2% to 5%, some investors may decide:

“Why hold gold when I can earn 5% elsewhere?”

That sounds logical.

But markets rarely move in such a simple and predictable way.

If higher interest rates automatically meant lower gold prices, gold should fall every time central banks raise rates.

History shows that is not always what happens.

Opportunity cost is only part of the story.

If you want a deeper explanation of how interest rates can influence buying decisions, read our guide on how to decide when to buy gold.

Why Interest Rates Alone Do Not Tell the Full Story

Many investors focus only on headline interest rates.

But markets often look at something else as well:

Purchasing power.

Let’s use a simple example:

- Interest rate: 5%

- Inflation rate: 7%

You may be earning 5% on your money.

But if prices are rising by 7%, your purchasing power is still going backwards.

Even though your savings balance increases, it buys less.

That matters because investors care less about the number printed on a statement and more about what that money can actually buy.

This is one reason gold sometimes behaves differently from what many expect.

We cover this concept in more detail in our guide on real interest rates and gold prices.

Real Rates Matter More Than Headline Rates

- Real Interest Rate = Interest Rate − Inflation

- If inflation is 6% and rates are 4%, your real return is −2%

- Gold often performs best when real rates are low or negative

Read more → Real Interest Rates and Gold Prices

What Happened During Previous Rate-Hiking Cycles?

Many people assume:

Higher rates = lower gold prices

History tells a more complicated story.

At several points over the last 50 years, gold has risen even while interest rates were moving higher.

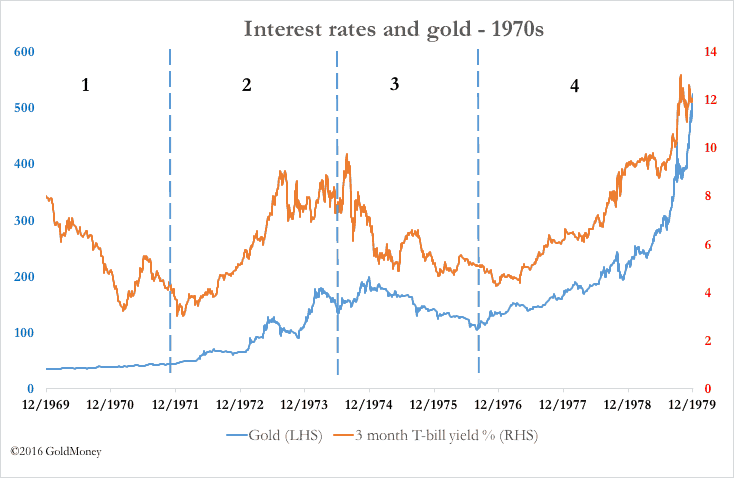

One of the clearest examples came during the 1970s.

During that period, policymakers raised rates aggressively as they tried to control inflation. Yet gold still moved sharply higher.

The 1970s

Gold moved from around US$35 per ounce at the start of the decade to over US$800 by 1980.

The lesson is not that rising rates are automatically bullish for gold.

The lesson is that interest rates are only one part of a much bigger picture.

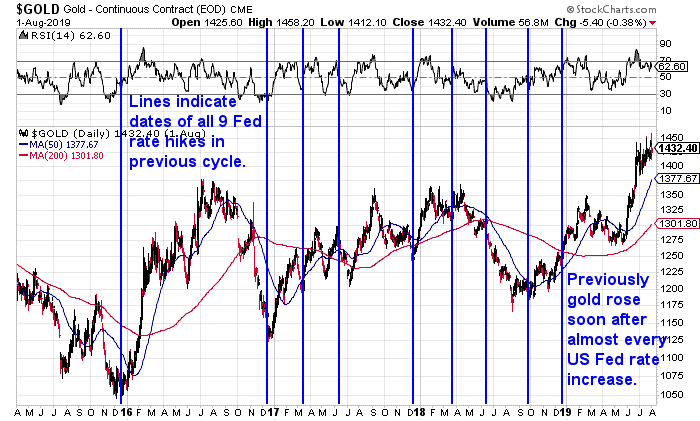

The 2004–2006 Federal Reserve hiking cycle

Between 2004 and 2006, the US Federal Reserve steadily increased rates.

Gold did not collapse. Instead, it continued moving higher.

More recent cycles

Markets have also seen periods where gold remained resilient while rates increased.

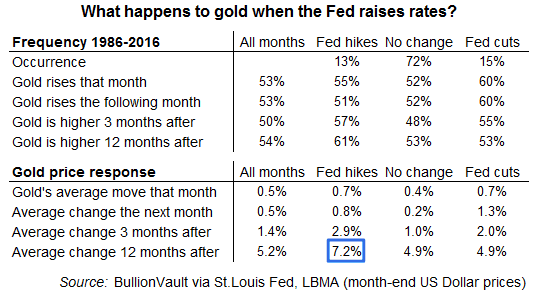

The data also suggests gold has historically performed better after rate hikes than many investors assume.

Why Gold Sometimes Rises Alongside Higher Rates

Several factors can influence gold at the same time.

Inflation may still be rising

Higher interest rates do not automatically mean inflation has been brought under control.

If inflation continues rising faster than interest earned on cash, investors may still look for ways to protect purchasing power.

Debt levels are much higher today

Governments, households and businesses now carry much more debt than in previous decades.

That matters because even small increases in rates can have a larger effect across the economy.

Rising debt levels can create pressures that extend beyond interest rates alone.

You can learn more in our guides on how the monetary system works.

Markets look ahead

Markets rarely wait for events to happen.

They often move based on expectations.

Gold can sometimes begin moving before central banks stop raising rates.

Financial stress can emerge

Aggressive rate increases can slow economic activity and put pressure on parts of the financial system.

That uncertainty can sometimes increase demand for defensive assets.

What Rising Rates May Mean Today

Recent Treasury yields have moved higher while gold has entered a period of consolidation.

At first glance that may seem negative for gold.

Higher yields can make cash and bonds look more attractive in the short term.

But markets often send mixed signals.

Rising debt, inflation concerns and broader economic uncertainty have not disappeared.

For a recent example, see our market update on rising bond yields and pressure on precious metals.

Short-term price movements do not always tell the full story.

For many investors, the bigger question becomes:

Should I buy gold now or wait?

What About Interest Rates in New Zealand?

The same principle applies in New Zealand.

Gold prices in NZ dollars do not automatically fall when the Reserve Bank raises interest rates.

Inflation, currency movements, global gold prices and investor sentiment can all influence outcomes.

That means New Zealand investors should avoid assuming that a higher Official Cash Rate automatically leads to lower gold prices.

If you’re following New Zealand-specific market conditions, see our guide on Should I Buy Gold Now or Wait?

Should You Wait for Interest Rates to Peak Before Buying Gold?

Trying to identify the exact top in interest rates can be difficult.

The challenge is that markets usually move before there is complete certainty.

By the time central banks officially stop raising rates, markets may already have adjusted.

This is one reason many investors focus less on finding the perfect moment and more on building positions over time.

We explore this further in our guide on when to buy gold or silver.

Frequently Asked Questions

Not always.

Gold has risen during several periods of increasing interest rates. Interest rates are only one factor affecting gold prices.

Higher rates can increase returns on cash and bonds, which may temporarily reduce demand for gold.

Gold also responds to inflation, debt levels, economic conditions and investor expectations.

Neither by themselves.

The broader economic environment often matters more than interest rates alone.

Not necessarily.

Markets often move before rate cycles end.

Gold and silver can respond differently depending on economic conditions, investor demand and industrial demand.

Read our comparison of gold vs silver.

Key Takeaways

- Rising interest rates do not automatically mean lower gold prices

- Interest rates are only one factor affecting gold

- Gold has risen during several previous rate-hiking cycles

- Inflation, debt and market expectations also influence gold prices

- Short-term price moves do not always reflect longer-term trends

Ready to Learn More?

If you’d like to continue learning, these guides may help:

- Should I Buy Gold Now or Wait?

- Real Interest Rates vs Gold Prices: What Can They Tell Us About When to Buy Gold?

- When Should You Buy Gold or Silver? A Strategic Guide for Every Wealth Stage

- Gold vs Silver: 7 Factors to Consider

If you’d like a quote or want to discuss your options, feel free to get in touch.

Or visit our shop to see what products are available to buy.

Editors note: This article was originally published 28 March 2018. Fully updated 25 May 2026.

Glenn's dedication to educating individuals on wealth protection through precious metals has helped over 2400 clients from New Zealand, Australia, USA and Europe to safeguard their financial futures. Passionate about financial independence and lifestyle freedom, Glenn’s mission is to empower others with the knowledge and tools to thrive in today’s volatile economic environment. When he's not advising on precious metals, Glenn enjoys spending time with his family and pursuing outdoor adventures.

Education: University of Auckland Bachelor of Science

Linkedin: https://www.linkedin.com/in/glenn-thomas-0984a4310/

- Watch What Central Banks Do, Not Just What Governments Say - July 22, 2026

- Gold Revaluation: Why the Debate Is Heating Up Again - July 20, 2026

- How the Centre of Gravity in the Gold Market Is Shifting East - July 15, 2026